The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

This article appeared first in The State of Fashion 2021, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company. To learn more and download a copy of the report, click here.

Global tourism had been growing strongly prior to the pandemic, a trend that contributed to the importance of travel retail and destination shopping for the global fashion industry. In fact, travel and tourism growth outpaced GDP growth over the past decade, driven by strong growth in the Asia-Pacific region. Before the pandemic struck, global airport sales were predicted to grow 6 percent in 2020. Now, of course, all of that has changed, and international arrivals globally are expected to drop by 60 to 80 percent in 2020.

Disruptions have profoundly impacted tourism hotspots and the fashion retailers operating in them. Destinations across the Southern Mediterranean sub-region of Europe and its periphery saw a 73 percent decline in international arrivals in the first half of the year, while those in the Northeast Asia sub-region posted an 83 percent decline. Across the board, popular destinations such as Thailand, Macau, Hong Kong and Singapore, all of which usually attract millions of tourists, saw very few arrivals. Hong Kong was particularly hard-hit, having welcomed 91 percent fewer tourists between January and September 2020 compared to the same period the year before.

Retailers in other major shopping hubs have also seen significant losses, as high-spending tourists from China, Russia and the Middle East stayed away from European fashion capitals like Paris, Milan and London. French luxury department store Galeries Lafayette said it was facing a €1 billion (approximately $1.17 billion) loss in 2020, while its Italian counterpart La Rinascente expected a 20 to 25 percent drop in annual revenues. “There are some great [shopping] districts around the world [but] it’s a real problem for districts to reinvent themselves [now],” said British department store Selfridges Group Managing Director Anne Pitcher.

ADVERTISEMENT

Retailers in other major shopping hubs have also seen significant losses, as high-spending tourists from China, Russia and the Middle East stayed away from European fashion capitals like Paris, Milan and London.

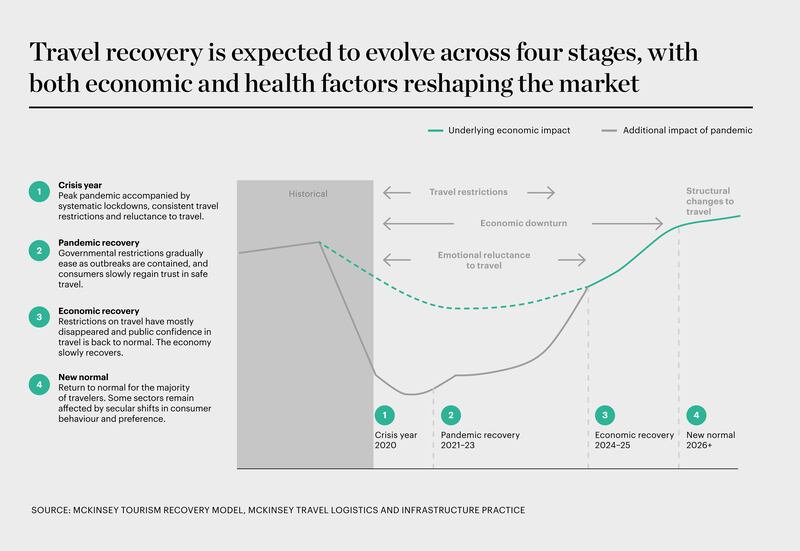

Scenario modelling by McKinsey and Oxford Economics suggests the pandemic lifecycle of the travel industry will consist of four stages: a crisis period, a recovery from the pandemic, a recovery from the economic downturn, then eventually a new normal, with the recovery’s timing and pace varying across regions (based on information available September 2020).

Uncertainty is expected to continue into 2021 and recovery will likely be focused initially on domestic and neighbouring-country travel. However, international tourism may not return to pre-pandemic levels before 2023 or 2024. This chimes with fashion executives’ sentiment about the recovery timeline for the travel retail sector. In our BoF-McKinsey State of Fashion 2021 Survey, 66 percent of executives expect it to take at least two to three years for travel retail sales to recover to their former growth levels.

The faster recovery of domestic and nearby -country travel already began to play out in 2020. In China and Europe, intra-regional travel picked up over the northern hemisphere summer, which saw a gradual increase in the number of flights. Booking of domestic flights in China recovered to pre-Covid levels in August and more than 600 million people travelled during China’s National Day Golden Week in October, providing some support to domestic retail. In North America, more than 90 percent of trips in August were undertaken by car, revealing the extent to which consumers shifted to domestic travel.

However, not all markets will recover at the same speed or to the same extent, as some are more dependent on global shoppers than others. The slower recovery of luxury sales in Europe compared to other geographies highlights the impact of absent luxury consumers, especially those who normally travel from China and other Asian countries. Even in a positive scenario, Europe is expected to see its luxury sales decline by 23 to 28 percent in 2021 compared to 2019 in the Earlier Recovery scenario.

With global travel hubs expected to remain relatively quiet throughout 2021, shopping at duty-free and luxury outlets will continue to shift towards China as retailers in these sectors double down on their efforts in the wider region. Swiss duty-free retailer Dufry, which was replaced as the world’s number one by China Tourism Group DF in 2020, plans to focus its recovery on Asia. In 2020, Hong Kong-based DFS Group acquired a 22 percent stake in Shenzhen Duty Free Ecommerce Co, signalling the growing importance of mainland hubs. Outlet player Value Retail said in April that China was a priority, after seeing strong growth in 2019 and in the period after lockdown in 2020.

“Mainland China has become the place where all the purchase power is trapped,” said Mauro Maggioni, Asia-Pacific CEO of Golden Goose. The Italian luxury sneaker and apparel brand is planning to open a store in Hainan, a tropical island in southern China, which is attracting major investment as a domestic tourism hub.

Given that footfall in destination stores and travel retailers will remain dampened by the decrease in tourists, brands will need to think creatively about how to address the “discovery problem” that will emerge in the customer’s path to purchase. In a bid to tackle this, some players are devising ways to get closer to their priority consumer groups. Brazilian beachwear brand Havaianas, for example, announced a $50 million investment to increase its footprint and visibility across the Asia-Pacific region.

Some players that have relied heavily on international tourism will continue to adjust their offerings to cater to the local market, in a bid to woo domestic customers. We therefore expect to see changes to assortments, in-store staff profiles and marketing. Galeries Lafayette, which previously generated 50 percent of revenue from international tourists, said it will focus on Parisians and French tourists for the 2020 holiday season. US department store Bergdorf Goodman has similarly developed new initiatives targeting affluent New Yorkers, and started offering same-day delivery to the Hamptons during the summer.

ADVERTISEMENT

Meanwhile, retailers with a high share of products associated with holidays and travel will continue to adapt their offerings. Samsonite Group, for example, has said it will shift away from suitcases and towards everyday products like day-to-day bags. Luxury brand Rimowa started its own sunglasses line, extending its product range beyond its recognisable aluminium suitcases.

As consumers continue to settle into travel restrictions and ongoing social distancing measures in 2021, brands should develop short- and medium-term responses to this new environment and align their assortment with evolving consumer demands. They should carefully monitor regional trends to capture opportunities, such as new domestic travel patterns and short shopping trips.

But fashion brands should continue to prioritise engagement on a local level, both in their home markets to compensate for the lack of tourism and overseas to reach customers where recovery from the pandemic is gaining ground. Despite a positive outlook in China, brands should not make hasty decisions about the market; instead they should plan a strategic approach informed by the latest market intelligence that will differentiate them from their peers over the longer term.

Finally, executives must also start planning for a post-Covid world by ensuring that they will be able to capitalise on the excitement that is unleashed once the pandemic is over, as consumers return to long-haul destinations and large social gatherings such as weddings, festivals and cultural events.

The State of Fashion 2021 Report: Finding Promise in Perilous Times

The fifth annual State of Fashion report forecasts the continuation of tough trading conditions for the global fashion industry in 2021. Changing consumer behaviour and shifting markets will force companies to find their 'silver lining strategies' to unearth digital innovation and reimagine physical retail. Explore the 10 themes that will define the state of the fashion industry in 2021 and how to navigate uncertainty while unlocking new opportunities in the sector’s recovery.

Explore the full report here.

1.

Learning to Live with the Virus

2.

Diminished Demand Is Here to Stay

3.

The Digital Sprint Will Have Winners and Losers

4.

Consumers to Seek Justice in the Supply Chain

5.

Travel Disruption Will Redraw the Fashion Map

6.

Less Is More for Both Consumers and Brands

7.

Fashion Is Set for a Surge in M&A

8.

Keep Your Suppliers Close

9.

Rethinking Retail ROI

10.

The WFH Revolution Will Rewire the Workplace

Antitrust enforcers said Tapestry’s acquisition of Capri would raise prices on handbags and accessories in the affordable luxury sector, harming consumers.

As a push to maximise sales of its popular Samba model starts to weigh on its desirability, the German sportswear giant is betting on other retro sneaker styles to tap surging demand for the 1980s ‘Terrace’ look. But fashion cycles come and go, cautions Andrea Felsted.

The rental platform saw its stock soar last week after predicting it would hit a key profitability metric this year. A new marketing push and more robust inventory are the key to unlocking elusive growth, CEO Jenn Hyman tells BoF.

Nordstrom, Tod’s and L’Occitane are all pushing for privatisation. Ultimately, their fate will not be determined by whether they are under the scrutiny of public investors.