Op-Ed | Fashion Needs a New Business Model. Speed Is the Answer.

Fashion businesses need to move faster to remain competitive. But speeding up means more than chasing trends – brands must realign their entire supply chain to create both market and social value.

By

John Thorbeck

NEW YORK, United States — Disruptive retail innovation raises expectations for every consumer and investor, whether it’s faster product design, delivery on demand or heightened standards for sustainability. Do the economics of fashion, an industry beset by shrinking profit margins, wave after wave of store closures and endless executive shuffles, support this new narrative? The answer depends on speed – but for reasons that go well beyond keeping up with faster trend cycles.

Fashion does not suffer any lack of experts willing to diagnose its woes and opportunity. One report, by Cowen & Co., offers a breakaway perspective. The bank’s lead analysts, John Kernan and Oliver Chen, call out the conventional supply chain model as “dead.” The same report downgraded Calvin Klein and Tommy Hilfiger parent PVH for the first time in eight years. Although Calvin Klein sales increased by $876 million since 2013, profit declined over that period by $20 million. PVH’s inventory turns hit all-time lows, while total inventory hit all-time highs. Sales growth based on higher inventory risk, the analysts argued, is no longer acceptable.

As an alternative, they offered a new thesis: speed = value. Cowen demonstrates that even modest change in speed equates to gross margin improvement, a model which can be projected across the sector and to clothing and accessories. The scale for multi-year capital benefit is significant, as follows:

Supply chains must move faster if they are to be more responsive to accelerating changes in demand. More important than cutting weeks of time out of the design-to-delivery calendar is building a link between retail supply flexibility and market value. Citing work by Warren H. Hausman of Stanford University, the critical metric is capital based on process innovation that reduces finished goods' lead times from months to weeks.

The source of being fast is supply flexibility in the first mile of the supply chain, in contrast to last mile logistics. This means upstream management to delay – or postpone — finished goods commitments. The impact of this strategy is to reduce or remove fashion uncertainty and exploit much shorter working capital cycles.

Speed, tightly and newly coupled with data science, enables opportunity across each tier and partner of the supply chain. The financial value created by speed should be invested, in part, in social impact initiatives for sustainability, transparency and worker well-being.

Where the supply chain is getting it wrong

Gap is illustrative of the industry’s transformation, or lack thereof. The emergence of fast fashion is often blamed for Gap’s inability to compete. Since 2006, Gap’s sales (with Old Navy) have stalled around $16 billion through four chief executives, while Zara parent Inditex reported sales doubled to $32 billion. Inditex’s profit margin increased while Gap’s dropped.

More sales and more profit is a difference in business model, not fashion style.

The model for speed is not only cycle time and store turns; it is less inventory, markdowns and lost sales. That capital productivity is what eludes Gap. The decision earlier this year to split Old Navy from Gap is designed to defer to shareholders while pushing a fix for the business further into the future.

Nike is another example where primacy of speed has been declared but not achieved. Nike’s “triple double” initiative calls for doubling speed-to-market capability, alongside 2X product innovations and 2X direct-to-consumer sales. A sourcing partnership with Flex brought high expectations for automation and location together in Mexico. It failed due to excessive losses at Flex, and Nike’s inflexibility to adapt design and volume to more automated manufacturing. Flex, adept at making Apple products, could not accommodate footwear, or maybe Nike could not adapt its cost-first culture to Flex. Either way, the magnitude of losses for each is a cautionary tale for anyone who thinks near-shoring and automation will be achieved smoothly or soon. Nike’s third attempt to source in Mexico is beginning anew, a telling example that the obstacles to speed and agility are more than resources and talent.

If speed is the essential catalyst of market value, according to Cowen & Co, what are the elements to fully achieve it? In fact, there are three: speed, science and social impact.

ADVERTISEMENT

Speed

This capability must be understood in depth vs. soundbite. It is not, “do what you do faster,” or even “be like Zara.” It is not see now/buy now, weekly drops in store or online or direct-to-consumer. Critically, it is the reduction of uncertainty, high forecast accuracy and neutral or negative working capital.

Metrics for this kind of performance are not in the order book or same-store sales; rather, it is full price selling, replenishment in season at 90 percent or better and financial incentives shared across supplier partners. These metrics are not conventional or even commonly measured, but they are the new scorecard for a horse race based on speed.

Speed, in summary, is not an operational challenge in sourcing alone. It is a firm-wide cultural commitment to speed decision-making, to be responsive to trends and to synchronise and share value across partners.

Science

Let’s be clear what data science is not. It is not digitalisation. Digital connectivity for visibility and transaction management is to invest in a failing, inflexible process which minimises costs.

Bill Gates said it best: "The first rule of any technology used in a business is that automation applied to an efficient operation will magnify the efficiency. The second is that automation applied to an inefficient operation will magnify the inefficiency."

The inefficiency of low-cost sourcing is evident. The goal in speed is to remove excessive risk and capital forced upon relationships in each tier of the supply chain, and to ensure that digital assets match to physical benefits. Translated, that means more margin (numerator) at less inventory (denominator), thus delivering substantial ROI in an industry too willing to accept its low tech, low growth and low profit reputation.

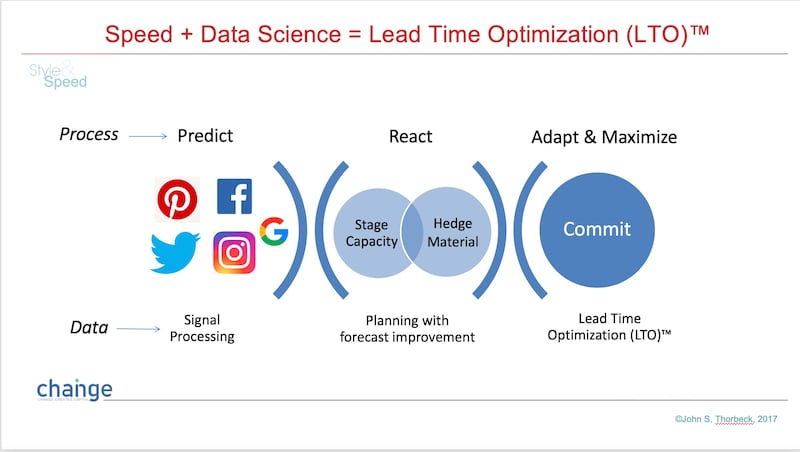

Data science is also not software automation, as if execution of speed and agility were standardised. Rather, it is iterative mining of data to achieve insights for how a business can excel or transform. Trend data from predictive analytics may offer insight into buyer intent, but value is limited without an ability to react. What good are real-time sales or search data when product cycles are still 40-plus weeks? What data science represents is a capability to reduce supply chain uncertainty by processing seeds and signals into insights which directly link to responsive suppliers. Speed and science are applied end-to-end via postponement, or what we call Lead Time Optimisation (LTO)™:

Lead Time Optimisation | Source: Courtesy Lead Time Optimisation | Source: Courtesy

Lead Time Optimisation | Source: Courtesy

Social Impact

Millennial demands for sustainability, transparency and zero waste are driving purchase decisions and loyalty. Speed is the key to de-risk high costs of uncertainty, and to unlock capital to invest in sustainability and worker lives. In an industry that is the most globalised, least efficient and yet largest employer of women worldwide, social and economic potential for women and supplier communities is dramatic. Women also account for 85 percent of fashion purchases, so the new narrative is more than CSR; it is the new basis for brand difference and meaning.

Cowen’s report states that retail’s financial status quo is unsustainable, and that the sector is desperate for a fresh strategic, investor and social narrative. Endless surveys of disruption are highly qualitative, yet quantifiable metrics to recognise meaningful value are missing. When so few retailers dominate industry profitability, and Amazon alone takes 50% of e-commerce growth, opportunity created by speed is unparalleled.

Fashion will right itself by recognising that digitalisation or experience or curation or personalisation are lagging the consumer’s own pace of change. What is underway is a magnitude of social change not limited to fashion alone. This generation demands that product value and values are inseparable. A Change Generation seeks to share technology and its benefits widely as a common good. The Millennial is both consumer and employee out to change the business of business. Together, they are a social movement.

Fashion must be the same.

John Thorbeck is the chairman of supply chain analytics firm Chainge Capital LLC.

The views expressed in Op-Ed pieces are those of the author and do not necessarily reflect the views of The Business of Fashion.

In 2020, like many companies, the $50 billion yoga apparel brand created a new department to improve internal diversity and inclusion, and to create a more equitable playing field for minorities. In interviews with BoF, 14 current and former employees said things only got worse.

For fashion’s private market investors, deal-making may provide less-than-ideal returns and raise questions about the long-term value creation opportunities across parts of the fashion industry, reports The State of Fashion 2024.

A blockbuster public listing should clear the way for other brands to try their luck. That, plus LVMH results and what else to watch for in the coming week.

L Catterton, the private-equity firm with close ties to LVMH and Bernard Arnault that’s preparing to take Birkenstock public, has become an investment giant in the consumer-goods space, with stakes in companies selling everything from fashion to pet food to tacos.