The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

The author has shared a YouTube video.

You will need to accept and consent to the use of cookies and similar technologies by our third-party partners (including: YouTube, Instagram or Twitter), in order to view embedded content in this article and others you may visit in future.

This article appeared first in The State of Fashion 2019, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company. To learn more and download a copy of the report, click here.

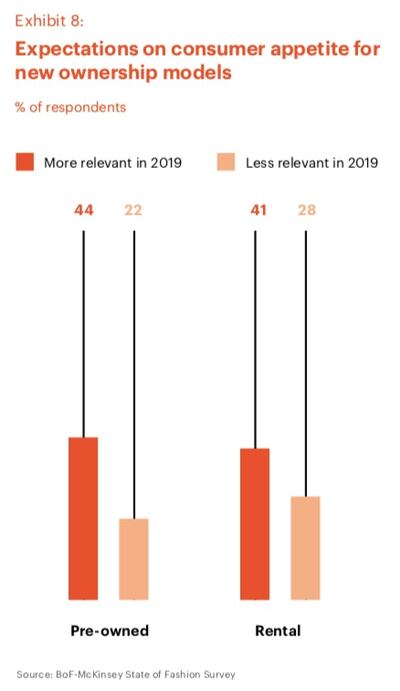

LONDON, United Kingdom — The lifespan of fashion products is being stretched as pre-owned, refurbished, repaired and rental business models continue to evolve. Across many categories consumers have demonstrated an appetite to shift away from traditional ownership to newer ways in which to access product.

In fashion, the shift to new ownership models is driven by growing consumer desire for variety, sustainability and affordability and sources suggest that the resale market, for instance, could be bigger than fast fashion within ten years. In recognition of this consumer shift, start-ups will not be the only players making their mark in these segments — established fashion brands will accelerate the pace with which they embrace new ownership models to further their relevance to consumers.

In more and more categories, consumers are choosing to rent rather than own goods outright. Think of Spotify supplanting CD sales and downloads, Netflix replacing video stores and ZipCar standing in for car ownership among many young urbanites. This is a fundamental evolution in consumer behaviour and we expect it will have an impact in the fashion business in the years ahead.

ADVERTISEMENT

New ownership models | Source: BoF-McKinsey State of Fashion Survey

This trend is partly driven by the young generation’s hunger for newness, while embracing sustainability. Research shows that the average person today buys 60 percent more items of clothing than they did 15 years ago.

But consumers keep that clothing for only half as long as they used to. For example, a survey done in Britain found that one in three young women consider clothes “old” after wearing them once or twice. One in seven consider it a fashion faux-pas to be photographed in an outfit twice. Simply put, young people today crave newness, and these cohorts are much more likely to embrace churn in their wardrobes. At the same time younger generations are more interested in sustainable clothing than older consumers. Rental, resale and refurbishment models lengthen the product lifecycle while offering the newness consumers desire.

Meanwhile, luxury brands are raising prices, significantly. Prices of fine watches and jewellery have nearly doubled since 2005. Tracking global prices of Louis Vuitton’s Speedy 30 handbag suggests an increase of approximately 19 percent per year since 2016. So, even consumers with six-figure incomes are looking to discounts and alternative models of acquisition for relief.

These demands are catalysing the successes of rental and pre-owned models. We expect that the ability of these players to satisfy a heightened desire for newness and an increased unattainability will bring them into the spotlight in 2019.

Luxury consumers can circumvent the price increases of the Speedy 30 bag, for example, through The RealReal, which was founded in 2011 and, as of May 2018, enjoys a $450 million valuation. It sells luxury brands, in gently used form, via a consignment model. The RealReal’s hook: top fashion brands, up to 90 percent off. It recently raised $115 million in a Series G funding round and plans to expand its brick and mortar presence in the US.

China’s YCloset takes a different approach, using a subscription rental model to grant customers access to an array of clothing and accessories free of additional charges. If the customer likes a particular piece, they have the option to buy it outright.

While established brands have traditionally turned a blind or scorning eye towards second-hand retail, they are now wading into the pre-owned and rental markets. For example, Stella McCartney launched a partnership with The RealReal in 2017, offering a $100 credit to consumers consigning her products on the platform. This can create a circular flow that encourages footfall in Stella McCartney stores, while building confidence in the quality and longevity of Stella McCartney products. Additionally, because of the circular nature of this partnership, it bolsters the corporate and social responsibility of the fashion brand.

ADVERTISEMENT

Other luxury players, such as Richemont, have purchased resale or rental businesses outright, to take control of how their products and brands are marketed on the secondary market.

The number of brands getting into the rental, resale and refurbishment business will increase markedly.

Some players have ventured into refurbishment, taking advantage of its sustainability benefits. Eileen Fisher, through its programme “Renew,” takes back gently-worn products, and either refurbishes them or uses the materials to create new products all together. Patagonia pioneered an in-house repair and resale model by buying back their own products and selling those used items at a discount price. On its website, Patagonia asserts, “The single best thing we can do for the planet is keep our gear in use longer and cut down on consumption.”

Express is betting on the rental market, launching “Express Style Trial,” which allows consumers to rent up to three items at any given time for a monthly fee. In an interview with CNBC, Express’ chief customer experience officer, Jim Hilt, states, “The consumer who is more interested in access versus ownership is happening across many industries. We looked at this evolution and asked, ‘how do we participate?’” In New York, French label Ba&sh is offering free rentals over a weekend period as part of its North America expansion strategy.

Turning to the year ahead, we expect 2019 will be known for three developments in particular. First, the number of brands getting into the rental, resale and refurbishment business will increase markedly; established players will progressively regard alternative ownership as a force they need to embrace or at least test through new collaboration models with retailers or start-ups in the sector. This will require careful business model considerations and a clear choice between partnerships, in-house development or M&A. Second, we predict a notable increase in the number of “rental native” brands born exclusively for rental or subscription models.

We would also not be surprised to see a unicorn in this space soon. Finally, more consumers will see a growing proportion of their wardrobes made up of pre-owned or rented products, especially for high-value items and accessories. While traditional players need not yet be alarmed, it will be essential to fully understand the emerging signals of what consumers prefer to own versus rent.

The company, under siege from Arkhouse Management Co. and Brigade Capital Management, doesn’t need the activists when it can be its own, writes Andrea Felsted.

As the German sportswear giant taps surging demand for its Samba and Gazelle sneakers, it’s also taking steps to spread its bets ahead of peak interest.

A profitable, multi-trillion dollar fashion industry populated with brands that generate minimal economic and environmental waste is within our reach, argues Lawrence Lenihan.

RFID technology has made self-checkout far more efficient than traditional scanning kiosks at retailers like Zara and Uniqlo, but the industry at large hesitates to fully embrace the innovation over concerns of theft and customer engagement.