The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

This article appeared first in The State of Fashion 2021, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company. To learn more and download a copy of the report, click here.

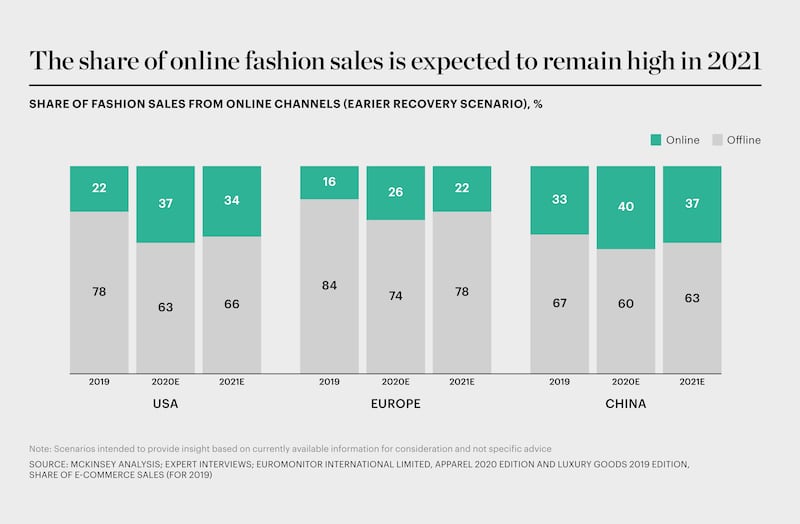

With the global pandemic keeping people at home, 2020 may be remembered as the year in which fashion retail made a definitive shift online. Over a period of just eight months, e-commerce’s share of fashion sales nearly doubled from 16 percent to 29 percent globally, jumping forward six years’ worth of growth. There are of course clear winners from this behavioural shift, with online marketplaces faring especially well. Zalando saw new customers rise by 39 percent year-on-year in April and Farfetch posted a 74 percent uplift in revenue in the second quarter, compared with the same period the previous year. Meanwhile, digital traffic to the websites of the top 100 European brands surged by 45 percent in April, compared with March.

The relative strength of digital channels was reflected in stock market performance too. While the fashion industry as a whole saw net declines in valuations, digital players were more resilient than their physical peers. From January to October, internet retailers had on average 42 percent higher valuations than other listed fashion companies, when indexing stock prices to December 2019. Adobe Analytics analysis of fashion e-commerce site visits shows the widening gap between the best and the rest. While overall US and EMEA digital revenues grew 24 percent year-on-year in the period of January to September 2020, the top 5 percent grew revenues 220 percent, while the bottom 25 percent declined by 2 percent.

70 percent of executives expect growth of more than 20 percent in their e-commerce channels.

Over the next year, momentum in e-commerce will only accelerate. Fashion executives see digital as the biggest opportunity by far for 2021, with 70 percent of executives expecting growth of more than 20 percent in their e-commerce channels. The trend will be led by China, followed by Europe and then the US — markets in which online sales are expected to grow 9-14 percent, 7-12 percent and approximately 3 percent respectively according to McKinsey Fashion Scenarios (based on information available September 2020).

ADVERTISEMENT

The dynamic e-commerce landscape in Southeast Asia is also expected to present fashion players with new opportunities. “We have been witnessing a profound structural shift to digital isation across our market,” said Forrest Li, the chief executive and co-founder of Sea Limited, during an earnings call in August 2020. Sea Limited owns Shopee, an online shopping platform, which has localised sites for Singapore, Indonesia, Vietnam, Thailand, Malaysia and the Philippines.

As online channels continue to prosper, it is likely that physical retail’s struggles will persist, and we expect to see fashion companies continuing to close stores in 2021. One example among many so far was Inditex’s announcement that it would close up to 1,200 stores worldwide and focus on digital growth. Diane von Furstenberg said it would close all of its stores and move to a digital-only model.

“Retail isn’t dead, but boring retail is dead,” said Rania Masri, chief transformation officer of Chalhoub Group, a Dubai-based retail and distribution company that partners with global luxury brands across the Middle East. “It’s always multi-layered, it’s not just about tech, it’s also about the people and how they work together in order to change and develop the experience we want to offer.”

To maximise impact amid a rapidly changing channel mix, fashion players must find new ways to excite customers and encourage them to engage online. History shows us that, in a disrupted macro environment characterised by shifts in consumer behaviour, excellent customer experience yields financial results as well as opportunities for companies to recalibrate their propositions. Following the 2008 global financial crisis, customer experience leaders posted three times higher shareholder returns than laggards. This is an important point for brand executives to appreciate because there is a new picture emerging around brand loyalty. During the coronavirus pandemic, consumers across countries have indicated they are willing to move away from their favourite brands and to experiment more. In fact, over 60 percent said they switched brands or retailers in the early part of the year.

In China, innovations such as livestream commerce have captured the imagination and helped to bridge the gap between physical and digital by bringing human interaction to the digital shopping experience. The trend started as early as 2016 with the launch of Alibaba’s Taobao Live. Three years later, Chinese livestream revenues amounted to $63 billion. They are set to rise to $138 billion in 2020, according to Coresight and iResearch, having been boosted significantly by lockdowns. The number of sellers on Taobao Live grew by 719 percent in February alone. Influencers have also proven their value in the livestreaming environment, in some cases generating more sales in a few hours than department stores do in a day.

“Customers are craving newness, and livestreaming is a safe and exciting way for us to deliver exactly that, especially at a time where some customers are not able to join us in stores,” Josie Zhang, president of Burberry China, explained in her introduction to Burberry’s Tmall livestream session in March 2020, which garnered 1.4 million views and resulted in many of the featured products selling out within an hour.

With so much buzz around the channel in China, it is little wonder that global brands, including Ralph Lauren, Levi’s and Burberry, have begun to experiment with it. However, luxury players are discovering that it is challenging to maintain a gilded and distinguished brand positioning while creating the kind of natural, chummy atmosphere that the medium requires. Nonetheless, we expect many fashion brands to continue to trial and refine livestream strategies for China in the year ahead.

Despite its early hiccups, Livestream is starting to gain traction outside of China, with US livestreaming revenues expected to hit $25 billion by 2023. Livestream commerce is also likely to accelerate in 2021 as big tech firms and social media innovations enable direct online checkouts. Instagram introduced in-app checkout for Instagram Live in August 2020 and TikTok hosted its first shoppable livestream in the same month.

ADVERTISEMENT

Other new digital opportunities are leading to creative solutions for marketing, design and new revenue streams across the fashion industry. A partnership between Ralph Lauren and Snap Inc., for example, will create virtual branded apparel for avatars, while other collaborations exist between fashion companies and video games. A deal between Louis Vuitton and the League of Legends introduced in-game skins designed by Creative Director Nicolas Ghesquière to accompany a real-world capsule collection, and Net-a-Porter in China launched Animal Crossing skins showcasing Spring/Summer collections of local brands, connected by QR codes linking to products on the e-tailer’s Tmall store. With no end in sight for the trend towards increased screen time and digital interaction, virtual fashion is likely to emerge as a not insignificant opportunity for brands both as a revenue stream and as a channel for product discovery.

In other emerging digital trends, messaging apps leveraging remote clienteling are proving their value in supporting consumer purchasing decisions. From Japan’s Line to Russia’s Telegram, the apps provide marketing, customer service and social commerce opportunities, tapping hundreds of millions of users. At the height of the pandemic, Chinese retailers capitalised on people’s desire for human interaction by publishing QR codes to link consumers with sales reps in hundreds of brand-based WeChat groups. In Brazil and other Latin American markets where WhatsApp is popular, offline retailers leveraged the app for remote shopping.

Where it is not possible to integrate human interaction into the digital experience, artificial intell igence (AI) is likely to play an increasingly prominent role in boosting conversion, giving customers the chance to experiment with virtual try-ons powered by augmented reality. Several brands are now using these formats, including some formerly digital-resistant luxury watch players such as Grand Seiko. The growing appetite for AI makes a lot of sense. Shopify found that conversion rates increased 250 percent for products that were supported by try-on technology.

To support the digital customer journey, many fashion companies are now investing to elevate omnichannel ecosystems across platforms. As retailer app downloads surge, brands are building next- generation apps featuring storytelling and elements that connect digital experiences to physical stores, such as in-store self-checkout. At Burberry’s “social retail store” in Shenzhen, China, omnichannel has been woven into the shopping experience; customers are rewarded with social currency for online and offline engagement on the brand’s WeChat’s mini- program — exchangeable for free menu items at the in-store café.

In the coming year, we expect brands to elevate the online customer experience even further, as digital is augmented with physical, and vice versa, in increasingly sophisticated ways. To power up e-commerce growth, the digital customer experience and behavioural insights will be the top two priorities for data and analytics in 2021, according to fashion executives. In addition, brands will leverage innovations including integration of social shopping, reviews, gamification and personalisation, aiming to create a richer digital experience. One departure from the past, however, is that fashion players will need to be much shrewder with their investments to focus on those innovations that deliver on the bottom line.

The State of Fashion 2021 Report: Finding Promise in Perilous Times

The fifth annual State of Fashion report forecasts the continuation of tough trading conditions for the global fashion industry in 2021. Changing consumer behaviour and shifting markets will force companies to find their 'silver lining strategies' to unearth digital innovation and reimagine physical retail. Explore the 10 themes that will define the state of the fashion industry in 2021 and how to navigate uncertainty while unlocking new opportunities in the sector’s recovery.

Explore the full report here.

1.

Learning to Live with the Virus

2.

Diminished Demand Is Here to Stay

3.

The Digital Sprint Will Have Winners and Losers

4.

Consumers to Seek Justice in the Supply Chain

5.

Travel Disruption Will Redraw the Fashion Map

6.

Less Is More for Both Consumers and Brands

7.

Fashion Is Set for a Surge in M&A

8.

Keep Your Suppliers Close

9.

Rethinking Retail ROI

10.

The WFH Revolution Will Rewire the Workplace

The British musician will collaborate with the Swiss brand on a collection of training apparel, and will serve as the face of their first collection to be released in August.

Designer brands including Gucci and Anya Hindmarch have been left millions of pounds out of pocket and some customers will not get refunds after the online fashion site collapsed owing more than £210m last month.

Antitrust enforcers said Tapestry’s acquisition of Capri would raise prices on handbags and accessories in the affordable luxury sector, harming consumers.

As a push to maximise sales of its popular Samba model starts to weigh on its desirability, the German sportswear giant is betting on other retro sneaker styles to tap surging demand for the 1980s ‘Terrace’ look. But fashion cycles come and go, cautions Andrea Felsted.