The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

Opens in new window

Opens in new windowPrivate equity (PE) firms looking to exit their fashion industry assets in 2024 may find they have some difficult choices to make. Against a backdrop of public market volatility, finding an attractive route to exit has been challenging, to such an extent that future deal-making may provide less-than-ideal returns and raise questions about the long-term value creation opportunities across parts of the fashion industry.

The significant shift in fashion’s financial market performance had, in fact, already started in 2018. Apparel, fashion and luxury (AF&L) companies generally tracked benchmark indexes closely up until then, after which industry performance began to diverge. While luxury companies outperformed the MSCI World Index by 14 percentage points in the five years to October 2023, non-luxury has underperformed the same index by 3 percentage points.

A similar scenario has been playing out in the private realm, with PE investors becoming increasingly cautious about non-luxury fashion categories, with deal volume stagnating over the last decade (except for 2021 which was a record PE deal year) even when “dry powder” — that is, capital available for investment — grew in the PE industry overall. In early 2023 amid an overall downward trajectory in the broader PE space, PE activity in AF&L ground to a halt due to pressure on discretionary consumer categories, high valuations and difficulties obtaining debt financing.

PE firms are likely to continue to see more limited exit options. On one side, strategic buyers have not made many investments in the past few years, given their caution around adding further complexity to their portfolios, and have focused instead on optimising their existing operations. PVH Corp and VF Corp, for example, last acquired targets in 2018 and 2020, respectively. On the other side, few PE-backed brands can reach the scale that an initial public offering requires. This then means attracting another PE investor, but they will likely be confronting the same concerns about the industry’s long-term value creation as the public market.

ADVERTISEMENT

An increasingly important priority for investors is to minimise exposure to the “fashion risk” inherent in brands that rely on actively shaping or getting fashion trends right. Naturally, these brands see swings in popularity over time, which makes it difficult to assess their value at any point in time, encouraging investors towards brands with iconic, timeless designs and a credible, compelling brand story. Even if investors are able to identify the brands with staying power, the added challenge of how to underwrite the intangible value — that is the value of the brand — adds complexity and risk to the deal-making process.

PE players have long homed in on luxury targets, for example the sale in August 2023 of luxury womenswear brand Zimmermann to PE firm Advent International. However, large luxury houses and other strategic suitors are equally attracted to these assets and are typically also active bidders when brands come onto the market.

PE firms are also not singularly focused on luxury — sportswear, footwear, wellness, outdoor, modern jewellery and intimates are on their radars too. Also in demand are B2B players further down the value chain that allow PE investors to gain exposure to the fashion industry indirectly (without assuming fashion risk). Transactions in this space include Permira’s acquisition of luxury contract manufacturer Gruppo Florence in late 2022 and San Quirico’s 75 percent purchase of Minerva Hub, a metallic components and leather producer for luxury companies, in 2023.

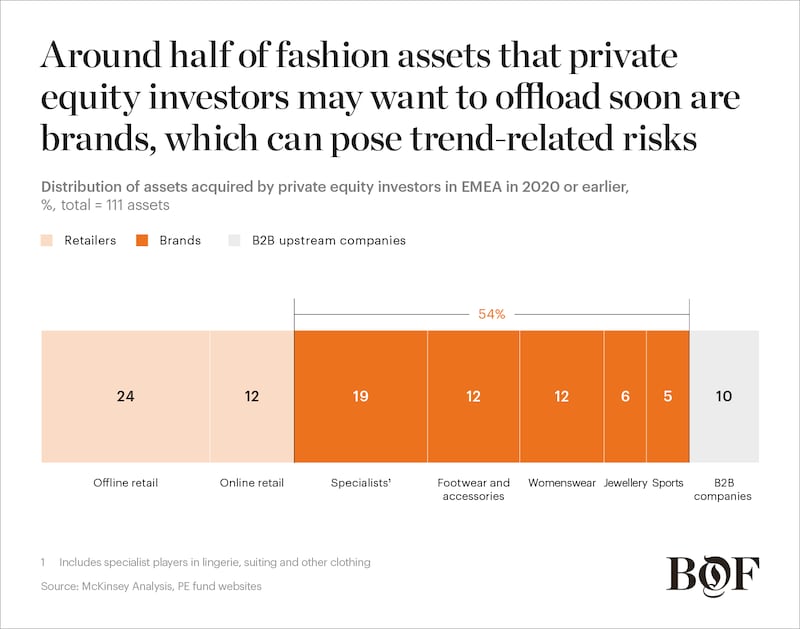

Across the PE industry, there is a growing backlog of deals that have exceeded their typical holding periods and need a sale to realise returns for investors. However, about half of the assets that are at or near the end of their holding periods are in segments which investors are increasingly wary of. Fashion-focused women’s apparel currently makes up 12 percent of this cohort in EMEA and poses a significant amount of trend-related risk. A number of potential deals in this category have stalled in 2023, including Giuseppe Zanotti (L Catterton), Sezane (General Atlantic), Isabel Marant (Montefiore Investment) and Ganni (L Catterton).

In the current economic climate, PE investors are also likely to be cautious about department stores and other “third-party” retailer assets (e.g. online and offline retailers that primarily sell goods from other brands), amid increasing macroeconomic headwinds and narrow profit margins. Third-party retail accounts for 36 percent of assets held (offline 24 percent and online 12 percent).

All told, PE firms’ choice may come down to delaying exit or compromising on price. But PE firms could also decide to sell to brand management groups, some of which have started making acquisitions. Authentic Brands Group, which bought Reebok in 2022, as well as WHP and Blue Star Alliance, are among such acquirers specialising in turning around distressed assets. However, the prices on offer are not always going to be attractive.

If investors cannot sell into private markets, they may look to the public markets for their exit. Since the 1980s, there were on average two to four AF&L IPOs in Europe and North America every year. The number of AF&L IPOs spiked in 2019 as well as 2021, with 25 IPOs over those two years, and have included brands such as Zegna, Allbirds, Dr Martens as well as luxury marketplace The RealReal.

But the performance of newly listed AF&L stocks has generally been challenging. Since 2018, the stock price of newly floated AF&L companies has dropped an average of 40 percent one year after listing, according to data from McKinsey Corporate Performance Analytics. Exceptions include USWE (IPO in 2021), Revolve (2019) and Levi Strauss (2018).

ADVERTISEMENT

As of the third quarter of 2023, the stock prices of nearly all AF&L companies that had IPOs in 2021 were below their listing prices. An outlier is On, whose share price has turned a corner and is now trading close to its listing value. Another exception from 2021′s IPO group is Zegna, whose shares at the end of September 2023 were up 13 percent.

Several factors have contributed to the outperformance of Zegna and On. One is the strength of the brand story. The heritage of craftsmanship of Zegna, born in wool mills in Italy and deeply rooted in its local environment, aligned with consumers’ desire for high-quality fabrics. Furthermore, Zegna moved away from a reliance on formalwear towards classic but “quiet” collections in time for the quiet luxury boom in recent years.

Investors also reward consistent and strong top-line growth. On grew revenue more than 60 percent in both 2021 and 2022, driven by its highly innovative solutions and design that appeal to a broad group of customers looking for comfort. Zegna’s revenue grew 27 percent and 16 percent in those two years. Another factor is that strong performers sit within in-demand categories like luxury and sportswear. Luxury now makes up close to half of the industry’s total economic profit, having increased its economic profit 3.5 times from 2018 to 2022. Sportswear’s (including sports footwear) economic profit grew 1.7 times from 2018 to 2022, despite a 17 percent drop in 2022.

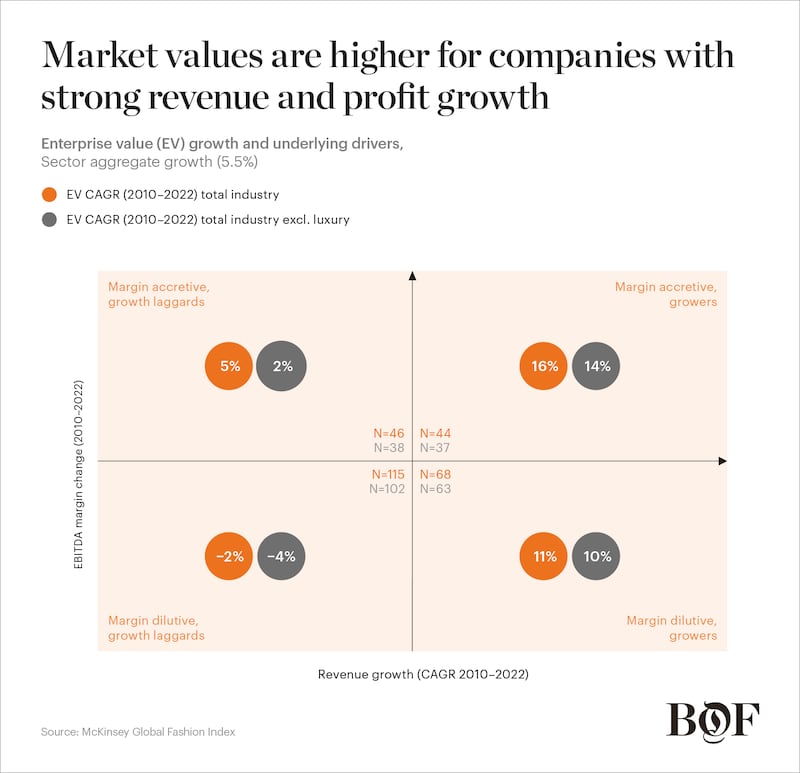

A McKinsey Global Fashion Index analysis in 2023 of publicly listed AF&L enterprise value between 2013 and 2023 suggests that while profitable growth is most attractive to investors, revenue growth is generally more heavily rewarded than margin accretion. Margin accretive companies that grew revenue above the industry average saw a 11 percentage points uplift in enterprise value growth, compared to margin accretive companies that grew below the industry average. In contrast, companies that grew revenue above the industry average only saw a 5 percentage points uplift if they were margin accretive compared to those that grew revenue but were margin dilutive.

Towards the end of 2023, there were many rumours of large IPOs for AF&L players, including Shein and Skims, raising expectations for a return of deal activity. One of the highest profile IPOs of 2023 was Birkenstock, whose target valuation set multiples at 18 times EBITDA. Despite very healthy margins of 35 percent EBITDA, this valuation would put Birkenstock at a similar or even higher multiple to LVMH (15 times EBITDA for the current year), and the same multiple as Nike, which has lower margins. Other shoe brands, such as Crocs and Dr Martens, are trading at six to seven times EBITDA. Despite the wave of brand hype generated by the “Barbie” movie (in which the shoe had a cameo) and strong performance fundamentals, Birkenstock stock declined in value in the first week of trading. This was due to investor concerns over how long Birkenstock can sustain its growth trajectory — to date driven by demand for comfort “home shoes” during the pandemic and made cool by high-end designer collaborations with Dior, Manolo Blahnik, Jil Sander and Proenza Schouler.

For successful flotations, firms are expected to meet several requirements, including a compelling equity story, sustained revenue and margin growth, ability to scale, and resilience amid category tailwinds. Of course, even these may not guarantee success. Consistent performance in meeting (and exceeding) investor expectations is critical to share price performance.

When deciding when to IPO, owners should closely monitor consumer trends and public perceptions, as well as the performance of recently listed companies. In addition, PE owners listing their portfolio companies will need to consider the impact of retaining a meaningful stake post IPO. By doing so, they expose themselves to share price volatility due to company performance, as well as broader market moves.

A public market revival is typically a precursor of PE deal-making and the funds with fashion specialisms are likely to move first. Non-fashion specialists are likely to remain on the sidelines for longer. Still, there are nascent signs of a more general shift in sentiment, with $1.2 billion of PE “dry powder” putting pressure on funds to begin investing again. Meanwhile, investment committees will look to the green shoots of M&A recovery, reflecting slightly better macroeconomic fundamentals in some markets and valuations starting to decline to more transactable levels.

ADVERTISEMENT

One thing is certain: given the volume of assets held by PE players, there is likely to be a queue for the exit when markets pick up, potentially creating a bottleneck. Within PE, aversion to fashion risk and concerns about discretionary categories are likely to remain significant barriers. Alongside market timing, value creation will likely remain a key priority for 2024. Owners should consider focusing on brand health, topline growth and commercial excellence (including getting pricing and promotions right), while also optimising sourcing, rethinking categories, and considering new occasions and channels. For those approaching exit, continuing to invest and not starving the assets is likely to be key, while at the same time hoping for consumer sentiment and discretionary spending to turn around.

This article first appeared in The State of Fashion 2024, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company.

The eighth annual State of Fashion report by The Business of Fashion and McKinsey & Company reveals an industry navigating deep uncertainty. Download the full report to understand the 10 themes that will define the industry and the opportunities for growth in the year ahead.

In 2020, like many companies, the $50 billion yoga apparel brand created a new department to improve internal diversity and inclusion, and to create a more equitable playing field for minorities. In interviews with BoF, 14 current and former employees said things only got worse.

A blockbuster public listing should clear the way for other brands to try their luck. That, plus LVMH results and what else to watch for in the coming week.

L Catterton, the private-equity firm with close ties to LVMH and Bernard Arnault that’s preparing to take Birkenstock public, has become an investment giant in the consumer-goods space, with stakes in companies selling everything from fashion to pet food to tacos.

Any fashion company that is contemplating going public needs to have not only the product and brand fundamentals right but also a business strategy that can easily be understood by the markets, writes Imran Amed.