The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

Many fashion executives were glad to leave 2020 behind, only to find that more challenges would lie ahead in 2021. Recent developments around more virulent mutations of Covid-19 and delayed vaccination programmes could further delay our path to herd immunity.

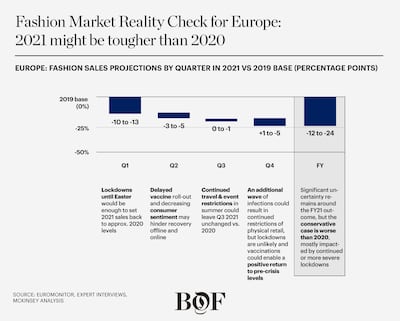

So the question nagging fashion executives now is how this will impact retail and the appetite for fashion in 2021. Market analysis by McKinsey & Company shows that the second year with Covid‑19 may well prove just as challenging for the fashion industry as 2020 — if not more so in some markets. New scenario analysis charting industry recovery against 2019 levels shows that the prospect of lockdowns continuing until Easter, which this year falls on April 4, could be enough to leave fashion retail in Europe worse off than last year, though the picture varies by region.

Across the board, fashion has been one of the industries hardest hit by the Covid-19 pandemic. Looking at full year 2020 results, European fashion sales were down roughly 20 percent on 2019 levels. But performance varied widely by market. Germany and France performed the best, down only 16-18 percent compared with 2019, while fashion sales in Spain, Italy, and some eastern European countries contract by a devastating 30 percent.

In the United States, fashion sales plummeted 23 percent year on year. China, by contrast, was quick to regain momentum, returning to a growth trajectory in August 2020 compared with 2019 levels, with full year results only down 7 percent year on year.

ADVERTISEMENT

But an especially strong market performance in the summer months in both Europe and the United States was an early indication of fashion’s capacity to rebound, offering a glimmer of hope for a sustained recovery ahead. Following the sharp collapse in demand, shoppers were eager to regain a sense of normalcy as stores reopened. In Germany, third-quarter revenue was only about 13 percent below 2019 levels, with peak weeks actually matching last year’s demand in the summer period.

Investments in building digital muscle are also paying off. E-commerce giant Zalando added 3 million new shoppers in the third quarter of 2020 alone, driving 30 percent year on year growth of its gross merchandise value (GMV).

Markets with a high e-commerce penetration, including the United States and the United Kingdom, reported growth of between 45 and 50 percent in e‑commerce in 2020, while more conservative southern Europe markets climbed by as much as 25 percent. Even China, where fashion e-commerce already has more than fifty percent market share, continues to grow in the high single digits.

So, while 2020 was tough, it provided an opportunity for the fashion industry to test its resilience, keeping consumers engaged and shopping through online channels while demonstrating its ability to rebound when high street stores re-open. But it has also painfully exposed the industry’s continued dependence on brick-and-mortar retail, an unnerving realisation given the prospects for continued lockdowns and restrictions in 2021.

Our projections for the remainder of 2021 are based on macroeconomic forecasts from the McKinsey Global Institute, along with our learnings from last year.

Europe: Down and out

Our outlook for 2021 is particularly downbeat in Europe, where it is conceivable that lost sales might range between 12 and 24 percent compared with 2019.

On first inspection, the picture may not seem quite so gloomy. It is true that 2020 has provided some assurance regarding the performance of sales during the summer months. After prolonged periods of lockdown, it is reasonable to expect a positive impact from pent-up demand. Although heavy restrictions are expected to continue suppressing international travel, fashion demand is expected to reach similar — perhaps even better — levels than in 2020 over the summer season. E-commerce will continue to perform strongly, as consumer sentiment should remain at least at 2020 levels, if not better, once lockdowns are lifted. Moreover, though another wave of infections and some continued restrictions in brick-and-mortar retail are likely to shape Autumn/Winter 2021 sales, advancing vaccination programmes should eliminate any need for further lockdowns by then.

ADVERTISEMENT

However, two key uncertainties remain. First, and most importantly, how bad will the first quarter really be? The extension of European lockdowns until Easter alone would be sufficient to set 2021 sales back to 2020 levels, or worse if there are further setbacks in the second half of the year.

Second, while it is still possible to avoid lockdowns in the fourth quarter, consumer sentiment remains highly uncertain. Public health measures such as the mandatory use of masks will likely still be required to keep transmission rates in check. As a result, our forecast growth range is wider around Easter and toward the end of the year, while we can be more confident about what to expect in the third quarter.

In the best case scenario, lockdowns of European retail stores would be lifted for the most part by mid-March and positive consumer sentiment in the fourth quarter would permit a partial recovery relative to 2019 later in the year. But if lockdowns continue until Easter, and there is only moderate consumption in summer, followed by a winter season with the pandemic still not fully contained, the recovery to pre-crisis levels would shift back to well into 2023.

United States: Improvements expected

The United States is expected to perform significantly better in 2021 than in 2020. Fashion sales will be down between 6 and 16 percent compared with 2019, but this is still a welcome improvement on 2020. This partial recovery will largely be driven by the continued surge of e-commerce, with online fashion sales set to outgrow pre-crises levels by as much as 40 percent. But while the United States has largely avoided renewed lockdowns of bricks-and-mortar retail, health and safety restrictions and limits on the number of people allowed in stores are expected to continue at least until the summer, and could possibly extend into the autumn.

China: A full recovery

Life in mainland China has largely returned to normal, so the most pressing question is really around the future of Chinese tourists, long the single most important source of income for the luxury industry in Europe. With a share of that consumption now being repatriated, luxury brands have proven remarkably creative in their efforts to capitalise on the resulting opportunity in the domestic market by creating shopping attractions, entertainment and special events. But when will Chinese travellers return to shop in global capitals?

One important consideration is the Chinese vaccination strategy: given the relatively low case numbers in China, some observers have argued that China will not distribute the vaccine at a high speed, which means Chinese travellers are unlikely to return in significant numbers before 2022. In the meantime, Chinese luxury consumers are expected to increase their spending at home by as much as 50 percent this year. However, that would only compensate for at most half of the sales lost overseas and in Hong Kong.

ADVERTISEMENT

Managing uncertainty in the road ahead

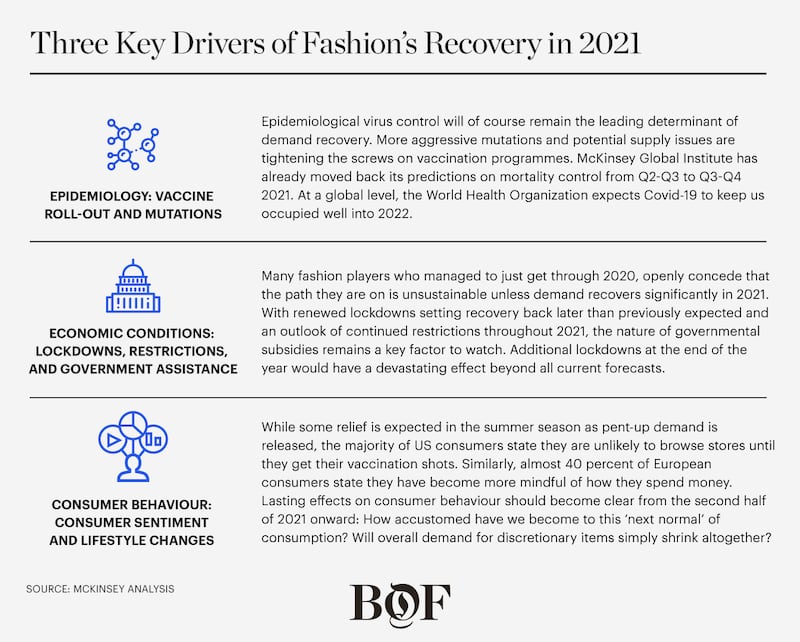

Though 2021 has only just begun and a high degree of uncertainty prevails, an analysis of recovery scenarios can provide fashion industry executives with a good starting point as they endeavour to plan ahead. Whatever the future holds, one thing is certain: stamina and perseverance will be key. Aside from the usual recommendations around building up e‑commerce channels and maximising agility and flexibility in planning, executives are well advised to keep their eye out for three key predictors of demand in 2021:

Overall, this reality check may leave some feeling cheerless about 2021 but there are evolving ideas such as the “roaring twenties” recovery scenario that has been bandied about, suggesting that people may decide to celebrate life as they did in the prosperous recovery period after the First World War. Could this spill over into consumer sentiment for the fashion industry? We can only hope. In the meantime, it is worth keeping an eye out for signs later this year that a significant upswing is coming in 2022.

Together, McKinsey and The Business of Fashion will continue to share our perspectives on how to manage uncertainties around Covid-19 throughout 2021.

Opens in new window

Opens in new windowRelated Articles:

The State of Fashion 2021 Report: Finding Promise in Perilous Times

The 10 Themes That Will Define the Fashion Agenda in 2021

The Year Ahead: Consumers to Seek Justice in the Supply Chain

From analysis of the global fashion and beauty industries to career and personal advice, BoF’s founder and CEO, Imran Amed, will be answering your questions on Sunday, February 18, 2024 during London Fashion Week.

The State of Fashion 2024 breaks down the 10 themes that will define the industry in the year ahead.

Imran Amed reviews the most important fashion stories of the year and shares his predictions on what this means for the industry in 2024.

After three days of inspiring talks, guests closed out BoF’s gathering for big thinkers with a black tie gala followed by an intimate performance from Rita Ora — guest starring Billy Porter.