The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

Opens in new window

Opens in new windowThis article first appeared in The State of Fashion: Beauty report, co-published by BoF and McKinsey & Company.

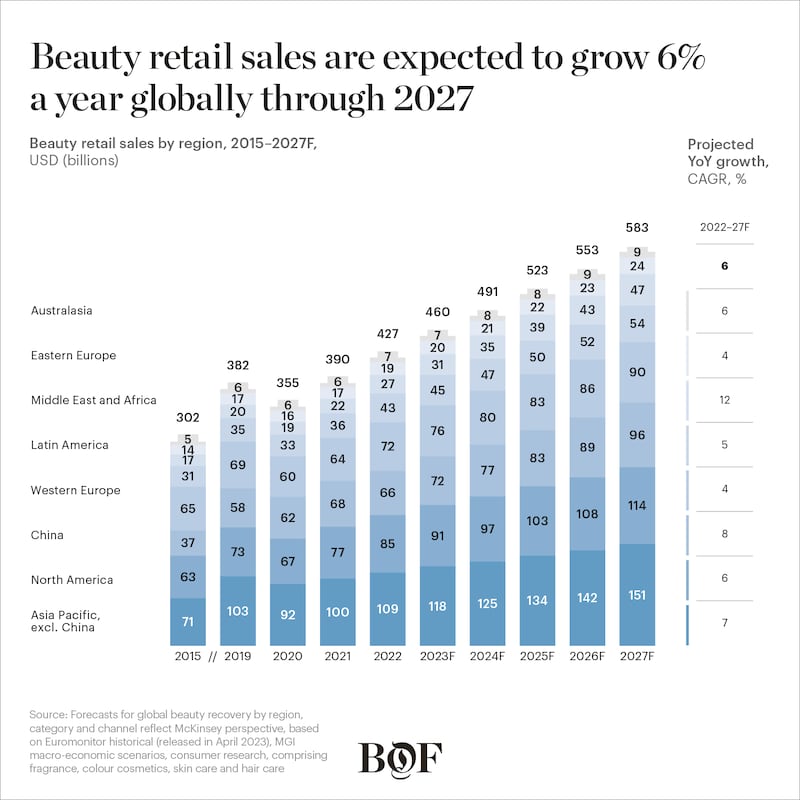

The global beauty industry will generate estimated retail sales of around $460 billion this year, a figure that is projected to increase to approximately $580 billion by 2027. With many beauty companies already recapturing their pre-pandemic lustre, the industry is expected to defy the downward pressures holding back other parts of the consumer sector in the short term.

But being part of that growth will require brands and retailers to deploy more sophisticated strategies than they did during the years preceding Covid-19′s upheaval. From intensifying competition to distribution channel pressures, times are changing. Beauty players that thrive amid these shifting pressures will be those that demonstrate a deep understanding of their unique value propositions as well as of their communities, with an ability to tirelessly lean into rapid innovation and product cycles.

Competition for wallet share will likely play out across more countries and regions than in previous years, and at different speeds.

ADVERTISEMENT

For example, China will likely remain a major market for beauty, but its compound annual growth rate is expected to slide to around 8 percent between 2022 and 2027, from 12 percent between 2015 and 2019. China will account for around one-sixth of global beauty retail sales by 2027, at $96 billion. The prestige segment holds the greatest potential in the country. Worth around $17 billion in 2022, the segment has an expected CAGR of around 10 percent to 2027. China’s luxury segment is smaller — approximately $4 billion in 2022 — but could see similar growth in the years to come. The greatest absolute growth will likely be in skin care, which will reach approximately $62 billion by 2027, up from around $45 billion in 2022.

Regionally, North America is poised to gain importance as a growth engine, accounting for $85 billion of the industry in 2022 and expected to reach approximately $115 billion by 2027. Notably, fragrance and hair care, worth $14 billion and $19 billion respectively in 2022, are expected to power the region with a CAGR of around 7 percent each over the five-year period.

Asia is another key region. Today, Asia Pacific, excluding China, is beauty’s biggest regional market, bolstered by Japan and South Korea, and will reach an estimated $151 billion in retail sales by 2027 from approximately $110 billion in 2022.

Europe, another regional stalwart representing about $90 billion in 2022, is expected to reach at least $115 billion by 2027. Similar to other parts of the world, consumers in both Western and Eastern Europe are trading up, with the increase in prestige spending experienced during the pandemic expected to continue driving high-end segments.

Growth opportunities in other markets are emerging as well. For instance, with an expected CAGR of 12 percent to reach $47 billion by 2027, the industry in the Middle East and Africa will continue to benefit from various regulatory and structural changes in select countries, including a lifting of foreign ownership rules that will ease entry into the region for global brands. India is also positioning itself for growth, with an expected CAGR of 8 percent to reach $21 billion by 2027, thanks in large part to shifting demographics and strong economic prospects helping to expand per capita spending on discretionary goods. Meanwhile, Latin America will likely continue to shake off the pandemic’s impact to return to growth, with CAGR between 2022 and 2027 rising to 5 percent to reach $54 billion.

Skin care, fragrance, colour cosmetics and hair care are all expected to power ahead at a combined global CAGR of 6 percent between 2022 and 2027.

Skin care, at around 45 percent of the sector’s total market value, remains beauty’s largest category. With an expected global CAGR of 6 percent, the category will grow from $190 billion in 2022 to $260 billion by 2027, with gross margins of between 50 percent and 70 percent. Innovation has been, and is expected to remain, a large driver in skin care growth, with brands increasing their focus on science-driven efficacy claims. Conglomerates have long dominated the category in key markets in Asia and North America, although challengers are also a source of competition. While mass is expected to remain the largest sub-segment, the greatest growth could come from luxury and prestige, with a CAGR of 11 percent and 7 percent over the five-year period respectively, reflecting the overall “premiumisation” of the category.

Fragrance — with global sales of around $70 billion in 2022 — is expected to see a CAGR of 7 percent, reaching close to $100 billion by 2027. The category is highly profitable, with margins of up to 90 percent in the luxury sub-segment and 80 percent in other sub-segments. Fragrance is expected to benefit from increasing penetration in China, where it accounts for less than 3 percent of the total beauty market. The category also has room to grow in the US, where it accounts for 16 percent of the total market, compared to Western Europe’s 26 percent. Mass and masstige segments will likely wane as consumers upgrade to higher-end segments, particularly niche fragrance brands. With increasing premiumisation, prestige fragrance has an expected CAGR of 8 percent and luxury fragrance 13 percent over the five-year period.

ADVERTISEMENT

Where does this leave colour cosmetics? Following a sharp drop during the pandemic, the category is expected to make a comeback in the next few years. After contracting — due to the pandemic, among other factors — at a CAGR of 1 percent between 2019 and 2022 to $80 billion, colour cosmetics will deliver 6 percent CAGR up to 2027, to more than $105 billion, with a generally even distribution across price segments. Brands, particularly those in the mass segment that rely on lower price points, should use the coming years to focus on profitability. With products in the category exhibiting lower average spend per order and requiring higher sampling expenses, this generally has resulted in the lowest average gross margins in the industry of between 45 percent and 60 percent.

Consumers are interested in adding products to their regular home beauty routines. More than half of consumers globally use three or more brands for skin care, hair care and fragrance, while one-third use five or more brands for cosmetics.

As for hair care, the $90 billion category today spans a broader product spectrum than traditional personal care shampoos and conditioners, which has helped it gain a greater presence in the beauty industry. Brands have an opportunity to benefit from a premiumisation and the “skinification” of hair, as consumers adopt multi-step hair care routines much as they have been doing with skin care. This includes an array of specialist products, creating a white space in beauty that traditional brands as well as new entrants can tap into, particularly given that consumers are more open to experimenting with buzzy, innovative products in hair care than in other categories. Hair care is expected to see the highest CAGRs in prestige and entry prestige, at around 11 percent and 8 percent respectively. Premiumisation in hair care also extends to adjacent products such as hair drying and styling devices. Hair care’s expected CAGR of 6 percent over the five-year period (excluding devices) will drive total retail sales to $120 billion, with gross margins of between 50 percent and 60 percent.

Industry growth strategies will need to reflect a shift in consumer behaviours with regards to hair, skin and body care. Consumers today are interested in adding products to their regular home beauty routines. More than half of respondents to McKinsey’s 2023 global consumer survey said they use three or more brands for skin care, hair care and fragrance, while one-third use five or more brands for cosmetics. At the same time, the survey — which canvassed shoppers across four generations in six countries (the US and China as well as the UK, Germany, France and Italy) — found approximately 40 percent of consumers indicated that they are loyal to brands they trust, while 69 percent said they like to try new products at least every six months. Certainly, consumers are diversifying within categories — in hair care, for example, consumers are expanding into specialised products for certain hair types, as well as scalp treatments, serums and oils.

Given consumers’ openness to trying new products, category opportunities are evolving and could provide entirely new growth avenues. Consider wellness: consumers are broadening their definition of beauty to a more holistic concept, encompassing a broad range of products, including probiotic skin care, supplements, beauty devices and home wellness. The shift towards wellbeing is also changing the profile of influencers in the space. While influencers and celebrities, as well as family and friends, continue to be a significant source of inspiration for beauty, shoppers also report being highly influenced by recommendations from doctors and dermatologists, according to the global consumer survey.

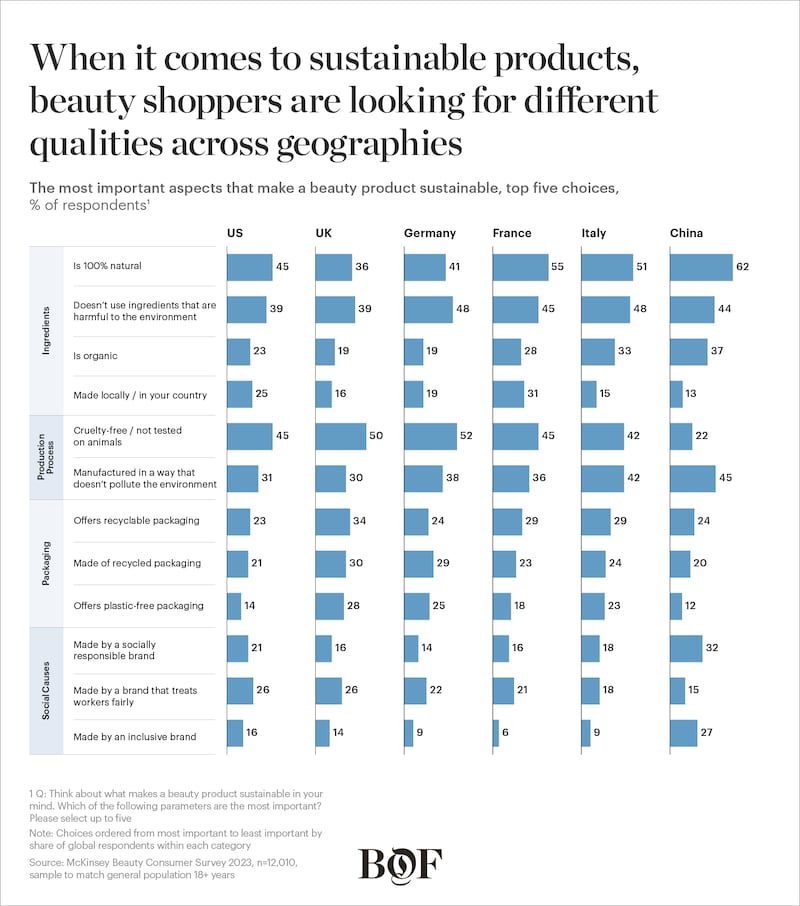

Across all these products, sustainability will be an overarching priority for many consumers. But there are multiple aspects of sustainable beauty products that players will need to consider. When McKinsey asked beauty consumers what aspects of sustainability matters most to them, the top overall responses were: the absence of ingredients that harm the environment, 100 percent natural formulas, and production that is cruelty-free and does not test on animals. But there were nuanced differences across the countries surveyed that brand strategies must factor in: Chinese respondents placed more emphasis on natural ingredients and environmentally friendly manufacturing, while those in the West also placed a high value on cruelty-free production. Overall, the focus on sustainability is most prominent among Millennials and Gen-Z, with more than half of the age groups reporting a willingness to pay more for beauty products from a sustainable brand.

Consumers’ embrace of e-commerce has defined beauty distribution around the world in recent years, and for good reason. Between 2015 and 2022, global e-commerce sales grew at a CAGR of 20 percent, with significant uptick during the pandemic. By 2022, digital shopping overtook speciality retail as the largest individual sales channel worldwide, accounting for around one-fifth of the industry’s overall total.

At a country and regional level, beauty’s distribution patterns are unfolding in different ways. E-commerce remains the largest channel in the US and is on track to represent around $45 billion in sales by 2027. Continued investment in beauty from e-commerce giant Amazon is boosting the online retailer’s influence in the market; Amazon is starting to reposition itself as a discovery channel rather than a replenishment platform.

The e-commerce heft of the US, however, is overshadowed by that of China. Digital sales in the country have gained share and now represent over 40 percent of the market, increasing to around $55 billion by 2027, when close to 60 percent of beauty sales in the country will be digital, driven by livestreaming and social commerce. While Tmall, China’s single largest sales channel, is expected to plateau, growing 2 percent annually in the five-year period, sales on social media platform Douyin (known as TikTok in Western markets) are expected to grow 11 percent.

ADVERTISEMENT

In the rest of Asia Pacific, as well as in Western Europe, beauty’s growth through 2027 will be more evenly distributed across all sales channels, including speciality and drug stores. Hypermarkets and discounters are also investing in mass and masstige beauty in the US and Europe, with Walmart, for instance, expanding its offering in relevant markets.

It is now clear that the beauty sector moves fluidly across physical and digital sales channels. Between 2022 and 2027, global e-commerce beauty sales will grow at an approximate CAGR of 12 percent, while physical retailers can expect a CAGR of 7 percent in speciality retail and 4 percent for drugstores and grocery stores.

Consumers now expect a mix of distribution channels. Both online and in-store channels are popular sources of beauty inspiration across regions and age groups, as McKinsey’s survey shows, with respondents ranking online and in-store as among the most preferred channels, at 40 percent and 45 percent respectively.

The industry’s attractiveness has not been lost on large, non-beauty businesses — including luxury megabrands that are launching beauty brands of their own, setting up funds and incubators, or acquiring established brands that offer differentiating products, large fan bases and a finger on the pulse of the next big thing.

Beauty has cemented its reputation as a stand-out industry given its proven resiliency and ability to consistently deliver high margins. But there’s another element that brands and retailers must not overlook — the enormity of the opportunities that emerging segments and sub-segments have to offer, from wellness to ultra-luxury, as well as geographically in, for example, the Middle East and India. Amid all this, profitable and sustained growth over the coming years will hinge on turbocharged innovation. Brand portfolios need to adapt to rapid product lifecycles, with “hero” products no longer the primary way to win with customers. Competition is intensifying, as is consumer desire to put to work a full range of beauty products that help them to look and feel their best.

For a deeper look into the report, join us for the global livestream of The Business of Beauty Global Forum on May 30 and 31, 2023. Click here for all the details on how to sign up.

The special edition of The State of Fashion report by BoF and McKinsey & Company explores the reshaping of the global beauty industry. Download the full report to learn about the key dynamics that will impact all categories in the years ahead, from the rise of wellness to the influence of Gen-Z.

This month, BoF Careers provides essential sector insights to help beauty professionals decode the industry’s creative landscape.

The skincare-to-smoothie pipeline arrives.

Puig and Space NK are cashing in on their ability to tap the growth of hot new products, while L’Occitane, Olaplex and The Estée Lauder Companies are discovering how quickly the shine can come off even the biggest brands.

Demand for the drugs has proven insatiable. Shortages have left patients already on the medications searching for their next dose and stymied new starters.