The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

Opens in new window

Opens in new windowThe global fashion industry sharply rebounded in 2021 and much of 2022. But in today’s fragile market, expectations of a continued recovery can downshift quickly. Fashion executives are largely pessimistic about the year ahead, anticipating that a number of challenges will negatively impact their businesses and customers.

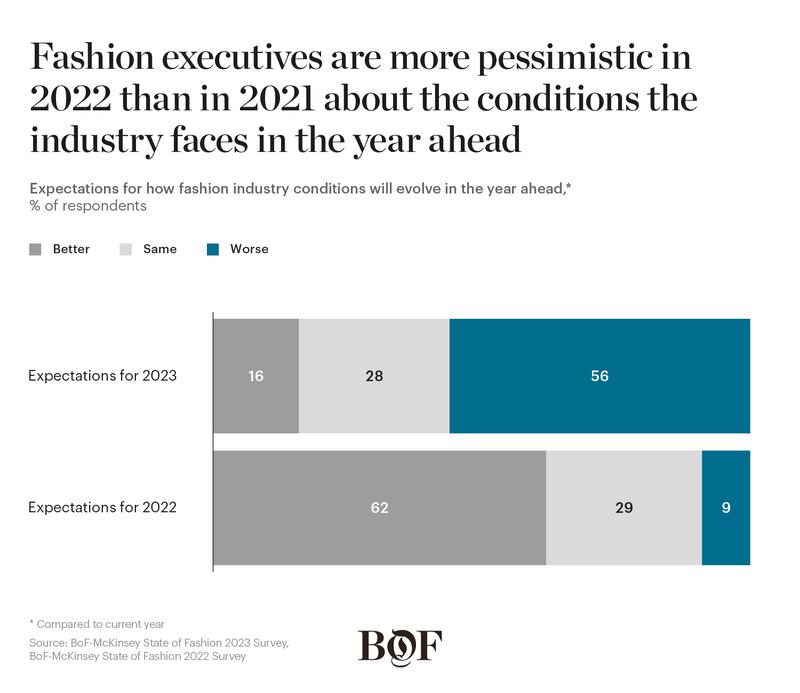

In the BoF-McKinsey State of Fashion 2023 Survey, 84 percent of industry leaders said they expect market conditions to decline or stay the same in 2023. The response stands in stark contrast to the cautious optimism the cohort felt heading into 2022, when 91 percent of executives predicted market conditions would improve or remain the same.

The effects of inflation are weighing heavy on executives as they look to 2023. With prices in Europe and the US reaching historic highs in late 2022 and central banks raising interest rates, consumer demand is expected to suffer. Inflation is also pressuring brands’ costs, as the industry encounters a competitive labour market and the consequences of climbing energy prices.

Beyond inflation, surveyed fashion executives identified a range of concerns that had not impacted the industry for the better part of a decade. In the year ahead, industry leaders are worried about geopolitical instability and conflict, supply chain disruptions, increased economic volatility, and rising energy prices.

ADVERTISEMENT

Regarding geopolitical tensions, respondents specifically referenced the war in Ukraine that began in February 2022. At the same time, only 5 percent of executives listed Covid-19 among their top three concerns in 2023, demonstrating the public health crisis has been eclipsed by economic and geopolitical issues.

Outlooks for 2023 vary by region and continent, however. In the US, which is more insulated from the effects of the war in Ukraine and Covid-19, 61 percent of executives expected the same or better conditions in 2023 than 2022. European and Asian fashion leaders were the most pessimistic, with 64 percent and 53 percent anticipating worsening conditions, respectively.

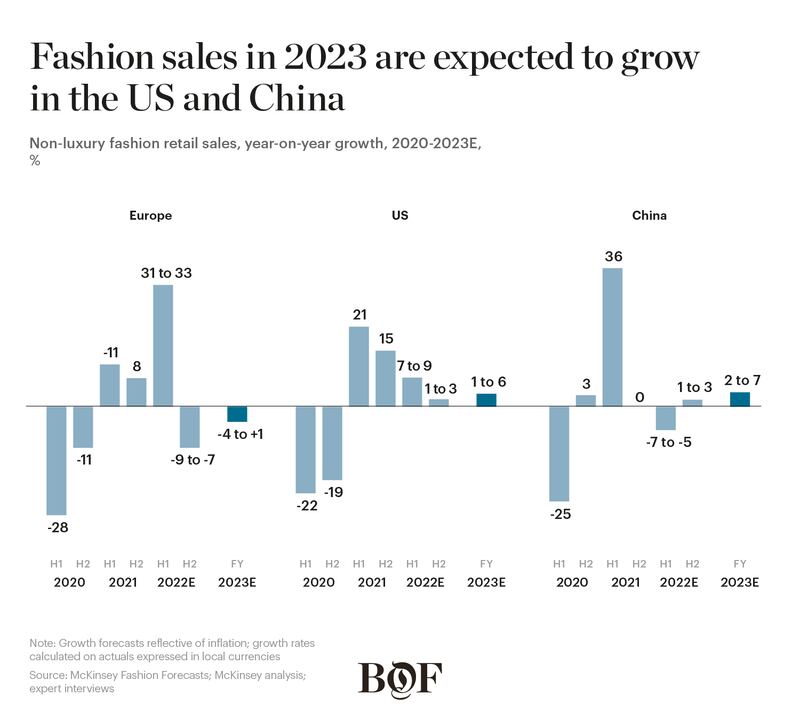

The sober outlooks are warranted. In 2023, the industry’s sales are expected to grow at a slower rate than in 2022, when the gains from the first half of 2022 were largely diminished by the deceleration in spending in the second half. Industry growth figures in 2023 will also be distorted by inflation, with a significant share of sales affected by rising costs and prices. In this context, 2023 could witness year-on-year volume declines, which has not happened for many years.

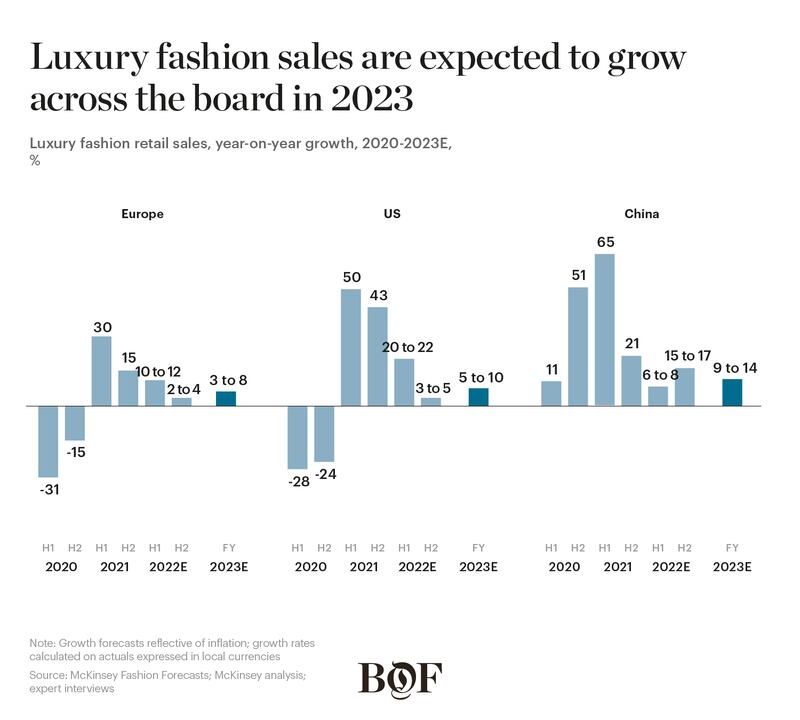

The luxury segment should show more resilience in the months ahead than other categories. Its sales are projected to grow 1 percent to 3 percent in the second half of 2022 and 5 percent to 10 percent in 2023, based on McKinsey Fashion Growth Forecasts. For the rest of the industry, growth in 2023 looks likely to be flat or even negative. While the industry is expected to contract between 5 percent and 7 percent in the second half of 2022, it should see slight improvements in 2023, with growth projected between negative 2 percent and positive 3 percent.

European prospects in 2023 are particularly gloomy. Europe’s GDP is expected to grow by less than 1 percent in 2023, and inflation is expected to remain high, undermining consumer confidence, which is already at levels as low as 2020. McKinsey’s Quarterly Consumer Pulse Survey found 14 percent of Europeans were optimistic about their country’s economic recovery in the second quarter of 2022, compared to 15 percent during the same period in 2020.

Non-luxury fashion sales in Europe are forecast to grow between negative 4 percent and positive 1 percent. And apparel and footwear will likely continue to lose wallet share among many consumers who are feeling the pinch of high petrol and energy prices and the tapering of pandemic-era government support programmes. Luxury will remain an exception in the region as wealthy consumers and tourists from the US and Middle East will be less affected by inflation. European sales for the sector are projected to grow 3 percent to 8 percent in 2023.

The US fashion industry’s growth will also likely slow, but might show greater resilience than Europe. The already-strong US dollar is likely to peak in the first half of 2023, and inflation is projected to cool by the second half. GDP in 2023 is forecast to grow 1.5 percent, down from 3 percent in 2022. Non-luxury fashion companies are expected to grow modestly in 2023, between 1 percent and 6 percent, continuing the trend observed in the second half of 2022. Like the rest of the luxury industry, US luxury companies should outperform other categories in the country, with forecasted growth of 5 percent to 10 percent. Travel will be a driver for the industry. Domestic leisure travel spending has already surpassed pre-pandemic levels and business travel is projected to recover to 96 percent of its pre-pandemic levels in 2023.

China is expected to see a modest recovery in 2023 after a difficult 2022, when persistent coronavirus outbreaks and a real estate crisis undermined the fashion market. The country’s performance in 2023 will be heavily correlated to GDP, which is forecast to grow between 5 percent and 7 percent. Non-luxury sales are projected to end 2022 with limited growth of 1 percent to 3 percent in the second half but are forecast to deliver 2 percent to 7 percent growth in 2023. After moderate growth in the first half of 2022, China’s luxury market should grow 15 percent to 17 percent year on year in the second half, and 9 percent to 14 percent in 2023. The country’s fashion industry performance at the end of 2022 and through 2023 will be heavily dependent on Covid-19 outbreaks and health precautions. China’s substantial middle class will also be highly impacted by policy responses to the real estate crisis and international travel guidelines.

ADVERTISEMENT

The majority of fashion leaders polled for the BoF-McKinsey State of Fashion 2023 Survey said they plan to focus on sales growth in the year ahead. But amid worsening economic conditions, 37 percent also said they plan to seek cost improvements. This marks the highest number of respondents looking to cut or better manage costs since The State of Fashion executive surveys began in 2016.

This comes as many of their biggest line-item costs are rising. More than 97 percent of respondents said they anticipate higher cost of goods sold as well as selling, general and administrative expenses in 2023. More than 50 percent of executives expect COGS to increase by over 5 percent, while 40 percent also expect SG&A to increase by over 5 percent. Furthermore, a higher number of leaders are planning to streamline their businesses in the year ahead than they were in late 2020 during the pandemic.

To protect margins, nearly three-quarters of executives stated that they plan to increase the prices of their products. Among respondents, 10 percent foresee price hikes of more than 10 percent.

To help mitigate the impacts of inflation on cost, over 60 percent of executives said they plan to optimise or re-negotiate sourcing agreements. In addition, approximately two-thirds of executives said they are considering nearshoring (moving production closer to their home markets) to adapt to unpredictable consumer demand. More than 60 percent of fashion leaders also said they were considering strategic partnerships with suppliers to increase their speed to market and create more efficient supply chains that will carry benefits for their businesses over the long term.

To reduce their own costs of inventory management and simplify sourcing agreements, nearly 75 percent of respondents aim to simplify inventory by reducing the number of products and styles, while 65 percent plan to adjust the balance between seasonal and basic items in assortments. Many fashion leaders are also anticipating customers will trade down to value products. As such, nearly 60 percent of respondents plan to increase the share of lower-priced items in their assortments, while 80 percent expect more than 10 percent of their sales in 2023 to be driven by promotions and discounts.

In 2023, fashion leaders anticipate a continuation of the casualisation trend that took hold during the pandemic as more shoppers shifted to working from home. Casualwear, followed by sportswear and sneakers, are the highest-ranking categories in terms of where executives see the greatest growth potential. Accessories, jewellery and formal shoes ranked lowest, reflecting expectations that consumers will cut spending on non-essential items during the period of economic uncertainty. However, while executives believe consumers will continue dressing casually in their day-to-day, nearly 40 percent expect occasion wear to be one of their top three growth categories in 2023, as special events like weddings increase after having been postponed during the pandemic.

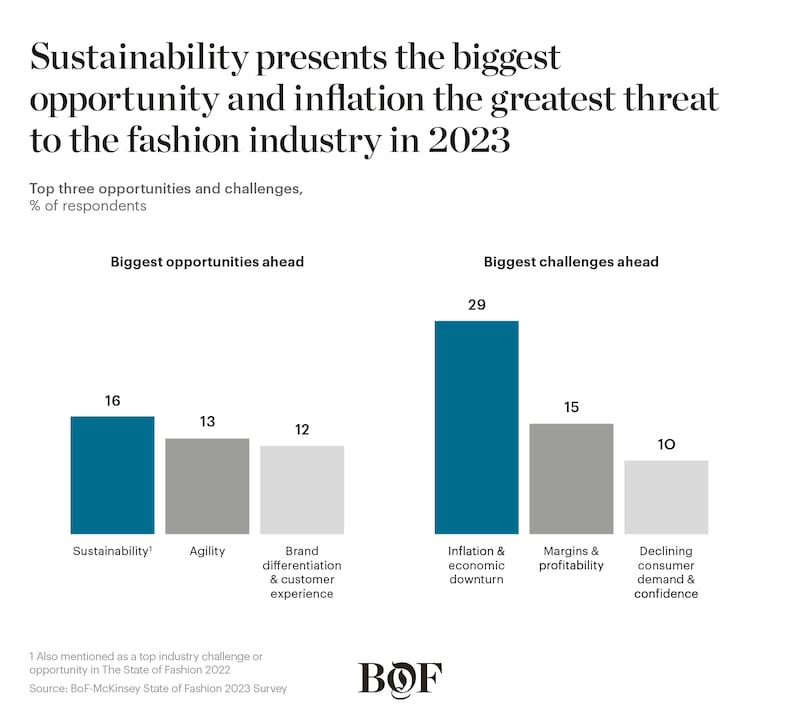

Despite the economic challenges ahead, some fashion executives said they remain focused on sustainability projects, which was cited as the most important opportunity for 2023 by 16 percent. Meanwhile, only 3 percent of respondents listed web3 as a top theme shaping 2023 and only 8 percent said it had been a major consideration for 2022. While metaverse-related initiatives will likely play a growing role in the industry in years to come, for now it is a nascent opportunity. Executives are more focused on addressing near-term challenges to their businesses.

As they consider where to invest in global markets, fashion executives cited the Middle East, North America and Asia Pacific (excluding China and India) as the most promising regions for 2023 compared to 2022. In line with more optimistic expectations in these regions, they were also among the top choices for respondents planning to increase their footprints in 2023.

ADVERTISEMENT

While executives are divided on how long the economic slowdown might last, they agree the conditions ahead will be difficult for the industry to navigate. In addition to concerns about inflation, economic slowdowns and margin pressures, respondents cited changing consumer demand and declining confidence as key challenges in 2023.

All told, the state of the global fashion industry in 2023 will be characterised by a sober world that is unpredictable and fragile. Fashion leaders will be challenged to streamline costs, quickly sharpen their risk management strategies and modernise their operations to build resilience amid a tumultuous time ahead.

The 10 fashion industry themes that will set the agenda in 2023:

1. Global Fragility

Amid the highest inflation in a generation, rising geopolitical tensions, climate crises and sinking consumer confidence in anticipation of an economic downturn, the global economy is in a volatile state. Fashion brands will need careful planning to navigate the many uncertainties and recessionary risks that lie ahead in 2023.

2. Regional Realities

Understanding where to invest globally has never been easy but rising geopolitical uncertainty and uneven post-pandemic economic recoveries, among other factors, will likely make it even more challenging in 2023. Brands can re-evaluate regional growth priorities and hone their strategies so they are more tailored to the geographies in which they operate.

3. Two-Track Spending

Consumers may be impacted differently by the potential economic turbulence in 2023. Depending on factors including disposable income levels, some will postpone or curtail discretionary purchases; others will seek out bargains, increasing demand for resale, rental and off-price. Fashion executives should adapt their business models to protect customer loyalty and avoid diluting their brands.

4. Fluid Fashion

Gender-fluid fashion is gaining greater traction amid changing consumer attitudes towards gender identity and expression. For many brands and retailers, the blurring of the lines between menswear and womenswear will require rethinking their product design, marketing, and in-store and digital shopping experiences.

5. Formalwear Reinvented

Formal attire is taking on new definitions as shoppers rethink how they dress for work, weddings and other special occasions. While offices and events will likely become more casual, special occasions may be dominated by statement-making outfits that consumers rent or buy to stand out when they do decide to dress up.

6. DTC Reckoning

Though brands across price segments and categories have embraced digital direct-to-consumer channels, mounting digital marketing costs and e-commerce readjustments have put the viability of the DTC model into question. To grow, brands will likely need to diversify their channel mix, including wholesale and third-party marketplaces, alongside DTC.

7. Tackling Greenwashing

As the industry continues to grapple with its damaging environmental and social impact, consumers, regulators and other stakeholders may increasingly scrutinise how brands communicate about their sustainability credentials. If brands are to avoid “greenwashing,” they must show that they are making meaningful and credible change while abiding by emerging regulatory requirements.

8. Future-Proofing Manufacturing

Continued disruptions in supply chains are a catalyst for a reconfiguration of global production. Textile manufacturers can create new supply chain models based around vertical integration, nearshoring and small-batch production, enabled by enhanced digitisation.

9. Digital Marketing Reloaded

Recent data rules are spurring a new chapter for digital marketing as customer targeting becomes less effective and more costly. Brands will embrace creative campaigns and new channels such as retail media networks and the metaverse to achieve greater ROI on marketing spend and gather valuable first-party data that can be leveraged to deepen customer relationships.

10. Organisation Overhaul

Successful execution of strategies in 2023 will in part hinge on a company’s alignment around key functions. Fashion executives need a new vision for what the organisation of the future will require, focusing on attracting and retaining top talent, as well as elevating teams and critical C-suite roles to execute on priorities like sustainability and digital acceleration.

This article first appeared in The State of Fashion 2023, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company.

Opens in new windowThe seventh annual State of Fashion report by The Business of Fashion and McKinsey & Company reveals the industry is heading for a global slowdown in 2023 as macroeconomic tensions and slumping consumer confidence chip away at 2022′s gains. Download the full report to understand the 10 themes that will define the industry and the opportunities for growth in the year ahead.

The global economy is in a fragile state. Geopolitical tensions, inflation and the climate crisis are heightening uncertainty and volatility — and weighing on consumer confidence. For fashion leaders, navigating this will require sharpened strategies.

From analysis of the global fashion and beauty industries to career and personal advice, BoF’s founder and CEO, Imran Amed, will be answering your questions on Sunday, February 18, 2024 during London Fashion Week.

The State of Fashion 2024 breaks down the 10 themes that will define the industry in the year ahead.

Imran Amed reviews the most important fashion stories of the year and shares his predictions on what this means for the industry in 2024.

After three days of inspiring talks, guests closed out BoF’s gathering for big thinkers with a black tie gala followed by an intimate performance from Rita Ora — guest starring Billy Porter.