The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

This article appeared first in The State of Fashion 2020 Coronavirus Update, an in-depth report focusing on the themes, issues and opportunities impacting the global fashion industry in the wake of the coronavirus, co-published by BoF and McKinsey & Company. To learn more and download your free copy of the report, click here.

LONDON, United Kingdom — If macroeconomic headwinds weren't already nudging businesses to reassess their position on a whole host of priorities, the coronavirus pandemic is now forcing companies across many sectors to make urgent, existential decisions. The global fashion industry is no different, with almost all companies battling lacklustre consumer confidence, foregone revenues and stores on lockdown.

Fashion companies — particularly those relying on longer lead times and inflexible supply chains — are uniquely vulnerable due to the category's discretionary nature. Indeed, fashion may face a harder time than discretionary goods overall: more than 70 percent of European and US consumers expect to cut back spending on apparel compared to a 40 to 50 percent drop in global discretionary spending.

A two-to-three-month lockdown will cause financial distress for 80 percent of European and North American fashion businesses, as volatility reduces investor confidence in a stock market facing its hardest hit since the global financial crisis of 2008.

ADVERTISEMENT

As the dust settles, the luxury sector may suffer more than other segments. This is due to the luxury sector’s reliance on travel retail (20 to 30 percent of industry revenue is generated from luxury purchases made outside consumers’ home countries), in addition to lower levels of online presence and high dependency on department stores and experiential in-store retail. For example, in March LVMH announced a 20 percent drop in quarterly revenue as a result of the Covid-19 outbreak. While the extent of the damage remains unclear, 2020 is already shaping up to be “the worst year in the history of modern luxury,” said Luca Solca, investment research analyst at Bernstein.

Consumption shifts already evident in countries from China to the US will be echoed across most major global markets.

Consumption shifts already evident in countries from China to the US will be echoed across most major global markets. In the US, 56 percent of consumers surveyed in McKinsey & Company's Covid-19 Consumer Pulse Survey said they are cutting back on spending, while 48 percent agreed that economic uncertainty is preventing them from committing to purchases they would otherwise have made. With the US reporting a record 6.6 million unemployment claims filed in one week between March 22 and 28, and Chinese unemployment figures at a record 5.7 percent in February, discretionary spending will take a backseat.

In the event that a vaccine is developed, some shoppers in certain markets might respond with a momentary "euphoric" spike in consumption, suggested Solca. This is similar to murmurings in China of a potential return of so-called "revenge buying," in which consumers may salve the wound of a months-long lockdown with feel-good spending. But "[if] we don't manage to vanquish the threat of Covid-19...the shape of recovery will be more subdued," he said.

Amid the health crisis, some digitally adept offerings and business models created pockets of positive momentum by cutting out middlemen and optimising e-commerce capabilities to reach self-isolating shoppers. At the same time, a “wellness dividend” has provided a boost for some hygiene-and health-orientated products and brands that have capitalised on the shift in consumer attention to safety, health and wellness. However, an indiscriminatory downturn in consumer appetite for discretionary purchases awaits even the savviest players, meaning any momentary uptick in sales will not be able to offset a decline in spending across the board.

While the duration of the pandemic remains uncertain, recovery will most likely be gradual. Consumer sentiment took up to two years to return to normal after previous global crises: recovery from the 2003 SARS pandemic, 9/11 and the 2008 financial crisis took 6 months, 1.5 years and 2 years respectively.

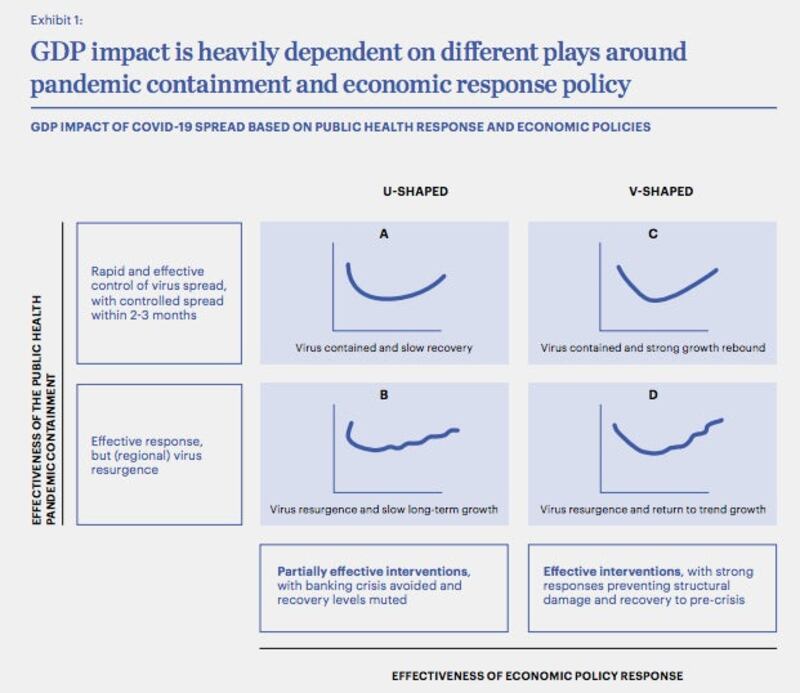

There are multiple possible scenarios for how the fallout will unfold, hinging on the effectiveness of different plays of pandemic containment and the ensuing economic response. The McKinsey Global Institute (MGI) describes four different scenarios for the crisis to develop (see Exhibit 1). In each scenario, the spread of Covid-19 is eventually controlled and catastrophic structural economic damage is avoided. Scenarios form a V-shape if economic rebound is strong, and a U-shape if economic recovery is slower. The recovery curves are distinguished further by the speed and effectiveness of the virus containment. However, any scenario will likely disproportionately affect the fashion industry given its discretionary nature, and the industry’s recovery will lag behind the rest of the economy.

As we have seen in China, the re-opening of physical retail does not mean business returns back to "normal." When 90 percent of apparel stores re-opened in China, footfall and purchases were still 50 to 60 percent below pre-crisis levels. Furthermore, each country will see varying recovery phases depending on their healthcare systems, financial resources and immediacy of response to the outbreak. For fashion, a rapid return of consumer confidence is especially important to restore the value chain.

We expect markets where the "dust has begun to settle," such as China and South Korea, to experience a quick recovery unless there are second waves of outbreaks. Although fears of a second wave in China are constant, with worrying signs of new small-scale outbreaks around the country at the time of writing. Developing countries in Asia, such as India and Indonesia, have been severely hit by the lockdown of production facilities, leaving millions without jobs and weakening their position in the global value chain. Similarly, we expect markets that have been under economic distress before the crisis — such as Venezuela and Nigeria — to require more time to restore growth, owing to their inherent political instability.

ADVERTISEMENT

In the west, there will be different rates of return of consumer confidence based on the speed and effectiveness of government support and how severely hit the country has been by the pandemic, with countries like Italy, Spain and France potentially faring worse than Germany.

Companies now need to consider actions for the recovery period and implement resiliency into their planning.

Looking ahead, businesses will have to review their operating models. While implementing short-term interventions — like cutting costs and production, securing liquidity and adjusting product assortments, which have been the highest priority in urgent reactions to the crisis — companies now need to consider actions for the recovery period and implement resiliency into their planning.

Companies must adopt a recovery position based on impact severity to help prepare for the deployment of a recovery action plan. This means reassessing their geographical footprint, store network and growth opportunities, while also looking for any emerging whitespace, be it during recovery or an extended crisis period. In The State of Fashion 2020 report, the biggest growth was predicted for emerging Asia, with rising opportunities in India and Southeast Asian nations like Indonesia. However, the preservation of these growth opportunities will depend largely on the way each country manages the pandemic. With a humanitarian crisis unfolding in emerging markets like India, fashion players will now need to re-evaluate strategies for which stores to re-open and when, and how their supply chain can best support the ramp-up.

In the event that collateral economic damage from the pandemic continues for an extended period of time, brands should review cost bases to identify measures for quick wins, set up employee plans to assess workforce decisions, and rationalise overhead spend to plan for potential store closures. On the supply chain side, fashion companies should learn from this global trade disruption that the value chain must be re-invented. This includes reviewing production regularly to identify potential disruptions before they happen in order to cushion the blow when they come to pass and strengthening regional integrated supply chains. It also means exploring nearshoring activities to bring flexibility and autonomy to their production facilities. Broadly speaking, non-core assets and activities should be divested and stopped to streamline current offerings and ensure efficient execution.

Speed and adaptability are of the essence for this crisis. But when the first signs of normalcy do begin to emerge, companies are cautioned not to be complacent. Instead, they must double-down on recovery and resiliency measures for this will be a time of unprecedented transformation for the global fashion industry. Only then can companies begin to decipher what their “new normal” actually looks like.

The Coach owner’s results will provide another opportunity to stick up for its acquisition of rival Capri. And the Met Gala will do its best to ignore the TikTok ban and labour strife at Conde Nast.

The former CFDA president sat down with BoF founder and editor-in-chief Imran Amed to discuss his remarkable life and career and how big business has changed the fashion industry.

Luxury brands need a broader pricing architecture that delivers meaningful value for all customers, writes Imran Amed.

Brands from Valentino to Prada and start-ups like Pulco Studios are vying to cash in on the racket sport’s aspirational aesthetic and affluent fanbase.