The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

This article appeared first in The State of Fashion 2019, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company. To learn more and download a copy of the report, click here.

LONDON, United Kingdom — After strong performance in 2018, the industry will slow slightly in 2019. The McKinsey Global Fashion Index predicts industry growth of 3.5 to 4.5 percent in 2019 compared with a 4 to 5 percent estimate for 2018. The weaker forecast reflects economic predictions for slightly slower global growth and potential disruption to trade relationships. We see Latin America, Middle East and Africa and Russia experiencing more economic and political challenges, which will likely dampen consumer spending. Europe is facing a slowdown and US growth may have peaked in 2018. Emerging Asia Pacific countries and much of emerging Europe, on the other hand, will continue to see strong spending growth with more global players entering these markets.

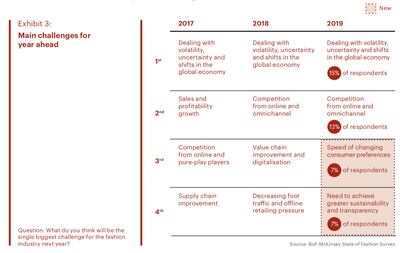

The caution in the economic outlook is also reflected in our BoF-McKinsey State of Fashion Survey, with 42 percent of respondents expecting conditions to become worse in 2019. Dealing with volatility, uncertainty and shifts in the global economy are seen as the top challenges for the third straight year. This pessimism could be driven by fears of an accelerating trade war as China and the US react to each other’s tariffs, uncertainty over how Brexit will play out (still unclear as we go to press), or just a feeling that a 10-year boom is now overdue to tip into recession.

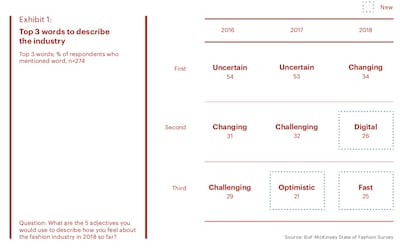

Top 3 words to describe the industry | BoF-McKinsey State of Fashion Survey

ADVERTISEMENT

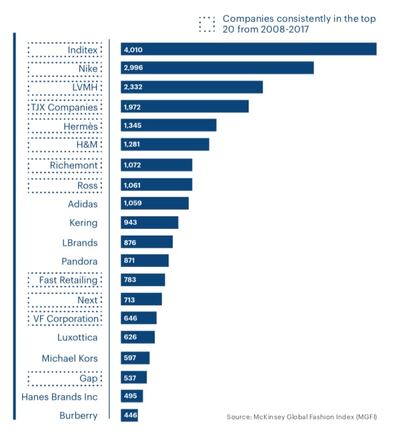

Over the past year, the global fashion industry has reached new heights. We see growth of 4 to 5 percent in 2018, slightly ahead of our projections for 2018, and a considerable uplift on the 2.5 to 3.5 percent seen in 2017. Better performance has been driven by strong demand for luxury and value brands, sales growth in the US amid tax cuts and growth in emerging markets. However, as we describe in the McKinsey Global Fashion Index, this recovery has been polarised. Most of the economic gains have accrued to the top 20 “winners,” most notably in the luxury segment, while a growing number of players are struggling to create economic value.

Still, better industry conditions on aggregate have brought an overall change in attitudes. Now used to uncertainty after living with it for so many years, in 2018 fashion executives have begun to think less about survival and much more actively about their strategic agenda. When asked in the BoF-McKinsey State of Fashion Survey to describe the industry, the word that comes to the minds of most executives (34 percent) is “changing.” The second and third most common words are “digital” and “fast.” The implication is that change has become a key priority among industry leaders, with a particular focus on digital and speed-to-market.

The attitudes of executives also reflect evolving consumer behaviours that are forcing industry players to “self-disrupt” (the #1 trend identified by executives for 2019.) Footfall in the physical environment continues to decline, which is driving the need for brands and retailers to develop their omnichannel strategies. Social media has an increasingly important voice in dictating consumer demand, and it is helping small brands grow explosively. Across the industry, speed-to-market and responsiveness to consumer needs are becoming critical success factors.

Top 20 players 2017, By economic profit, $US million

When asked to reflect on the importance of the trends we predicted in last year’s State of Fashion report, executives identified technology-related issues as their top four choices. Consumer shifts enabled by technology were particularly salient, with “mobile obsessed” cited as the most important of the trends we predicted. The second- and third-most important are “platforms first” and “start-up thinking,” again highlighting companies proactively dealing with digital disruption in the fashion system.

We were surprised to find artificial intelligence (AI) less highly ranked. This shift may not have reached critical mass in 2018, but we predict it will continue to affect the industry in 2019 and beyond. Players including Amazon, Alibaba, Myntra and Stitch Fix have made progress across various areas of the value chain and others will follow suit. Ananth Narayanan, chief executive of Myntra, remarked that, “for curation and assortment, we are using a lot more data science to tell what will sell. I think that could extend a lot more into manufacturing and the back-end system and we are doing parts of that already at Myntra.”

An increasingly important priority is sustainability and transparency, reflecting rising concerns on the part of consumers and companies about how to alleviate their impact on the environment. Sustainability, which for the first time breaks into our respondents’ list of the most important challenges, is evolving from a tick-box exercise into a transformational feature that is engrained in the business model and ethos of many recent success stories.

Main challenges for year ahead | Source: BoF-McKinsey State of Fashion Survey

ADVERTISEMENT

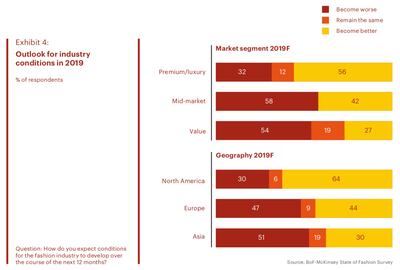

By geography, the most optimistic about the coming year are executives in North America. By segment, the most positive are executives from luxury brands, reflecting their strong growth trajectory in 2018. In all other regions and segments, executives are notably pessimistic, reflecting the potential challenges ahead. Not surprisingly, executives are looking to invest where they see the most need to add value. For the third year straight, the top sales growth investment priority remains developing omnichannel capabilities. This reinforces our perception that executives have finally come to terms with the fact that the industry is digitising, but are not yet satisfied with their own response. Some 54 percent of the BoF-McKinsey State of Fashion Survey respondents said increasing omnichannel integration (alongside investing in e-commerce and digital marketing) is their number one priority for 2019 for the third year running.

Outlook for industry conditions in 2019 | Source: BoF-McKinsey State of Fashion Survey

From an operational perspective, another persistent trend has been the desire to address cost structures at an organisational level, including efforts to improve productivity. This remains a key priority in 2019 with 29 percent of the BoF-McKinsey State of Fashion Survey respondents saying they wish to “review organisational structures and focus on increasing employee productivity.” This underlines the need to adapt operating models and create a more agile organisation that can thrive in the digital world.

Overall, the fashion industry continues to hover in a state of flux and the fortunes of individual players can turn with frightening speed. As our 10 trends indicate, new markets, new technologies and shifting consumer needs present opportunities but also risks. We predict that 2019 will be a year shaped by consumer shifts linked to technology, social causes and trust issues, alongside the potential disruption from geopolitical and macroeconomic events. Only those brands that accurately reflect the zeitgeist or have the courage to “self-disrupt” will emerge as winners.

The 10 trends that will set the agenda for the global fashion industry in 2019

Downward movements in key economic indicators and other potentially destabilising forces will conspire to create a more cautious mood. With the possibility of a global economic slowdown by 2020, companies will turn more prudent and start to look more aggressively into opportunities to boost productivity compared to previous years.

ADVERTISEMENT

India becomes a focal point for the fashion industry as its middle-class consumer base grows and manufacturing sector strengthens. Fashion players must redouble their efforts in this highly fragmented and challenging market where an educated and tech-savvy demographic rub shoulders with the poor and upwardly mobile.

3. Trade 2.0

All companies will need to prepare contingency plans to face a potential shake-up of global value chains. On the one hand, the apparel trade could be reshaped by new barriers, trade tensions and uncertainty and, on the other hand, by new opportunities from growing South-South trade and the renegotiation of trade agreements.

The lifespan of the fashion product is becoming more elastic as pre-owned, refurbished, repair and rental business models continue to evolve. Fashion players will increasingly tap into this market to gain access to new consumers seeking both affordability and a move away from the permanent ownership of clothing.

5. Getting Woke

Younger generations’ passion for social and environmental causes has reached critical mass, causing brands to become more fundamentally purpose-driven to attract both consumers and talent. Consumers from some but not all markets will reward players that take a strong stance on social and environmental issues beyond traditional CSR.

6. Now or Never

In the mobile consumer journey, the gap between discovery and purchase has become a pain-point for a more impatient fashion consumer, who seeks to purchase exactly the products they discover, immediately. Players will focus on bridging this gap through shorter lead times, improved availability of advertised products and new technologies such as visual search.

After years of having personal data owned and handled by businesses, a more distrusting consumer now expects companies to reciprocate with radical transparency and sharing of information. For companies to meet a new bar for consumer trust, they will need to offer a heightened level of transparency along dimensions such as value for money, creative integrity and data protection.

8. Self-Disrupt

Traditional brands are beginning to disrupt their own business models, image and offering in response to a new breed of small emerging brands that are accelerating thanks to decreasing brand loyalty and a growing appetite for newness. We expect more brands to follow suit on this path of self-disruption, which will have a significant impact on their operating models.

As the race to be the platform of choice for both customers and brands intensifies, e-commerce players will continue to innovate by adding profitable value-added services. Whether through acquisitions, investments or internal R&D, those players who diversify their ecosystem will strengthen their lead over those who remain pure players relying solely on retail margins.

10. On Demand

Automation and data analytics have enabled a new breed of start-ups to achieve agile made-to-order production. Mass players will begin to experiment next, responding more rapidly to trends and consumer demands, achieving just-in-time production and reducing overstock and making short, small-batch production cycles the new norm.

The LVMH-linked firm is betting its $545 million stake in the Italian shoemaker will yield the double-digit returns private equity typically seeks.

The Coach owner’s results will provide another opportunity to stick up for its acquisition of rival Capri. And the Met Gala will do its best to ignore the TikTok ban and labour strife at Conde Nast.

The former CFDA president sat down with BoF founder and editor-in-chief Imran Amed to discuss his remarkable life and career and how big business has changed the fashion industry.

Luxury brands need a broader pricing architecture that delivers meaningful value for all customers, writes Imran Amed.