The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

Selfridges is to join a stable of luxury department stores owned jointly by Thai retail conglomerate Central Group and Austrian property group Signa. Selfridges Group’s portfolio, which also includes Rinascente, Illum, Globus and KaDeWe, generated a pro-forma turnover of $5.6 billion in 2019 and is projected to grow to more than $7.9 billion by 2024.

But a recent study by Bain & Altagamma predicts that department stores will lose nearly half their share of global luxury goods sales from 2019 to 2025 as they face stiff competition from online players, specialty retailers and brands’ own direct-to-consumer channels. So what strategies are being deployed by the likes of Selfridges and its new owners to grow in a shrinking category?

Exclusivity over discounting

In recent years, the American department store sector has been on a race to the bottom as players tried to retain customers through heavy discounting. The results were catastrophic, not only antagonising brands but also pushing stores into bankruptcy.

ADVERTISEMENT

Many department store operators, including Selfridges, have shunned this strategy in favour of securing exclusivity with new brands or exclusive product drops with existing and more widely distributed brands thus giving shoppers a reason beyond price to visit their stores, online and off. A simple search on Selfridges’ website uncovers 1,129 exclusive items, and this is likely on top of the brands for which Selfridges is the exclusive retailer in London or the UK.

But exclusivity has its limits. Barneys was known to nurture fresh talent and for introducing the likes of Comme des Garçons, Yohji Yamamoto, Martin Margiela, Dries Van Noten, Prada, Ann Demeulemeester, Rick Owens and Alexander Wang to the US market, often in exchange for exclusive distribution rights. This gave the chain the allure of being cutting edge but often proved stifling for brands wishing to do more than stay stuck on the starting block. Producing exclusive drops for individual stores can also present challenges for brands depending on how easy it is for them to customise production and overcome minimum order requirements.

Reinventing store formats

Traditionally department stores have sought expansion by rolling out versions of their flagship format to secondary and tertiary cities, albeit often on a smaller scale. Prior to filing for bankruptcy in 2019, Barneys had 22 stores including its Madison Avenue flagship. The company had also tested various formats including Barneys Warehouse and Barneys CO-OP, the latter to attract a younger and more fashionable but less affluent crowd. Nevertheless, the department store operator over-stretched its balance sheet by expanding with formats that offered few points of difference. In addition to a rent hike at its Madison Avenue flagship, one of the last nails in its coffin was an expensive investment in a downtown outpost in Chelsea.

The issue most prestigious department stores have with new formats is that their identity is so closely linked to their mothership. This is especially the case with Harrods and its Knightsbridge site. The company has made numerous attempts to open new locations, including one across the street called 102. The store, featuring concessions such as Krispy Kreme and Yo! Sushi as well as florists, an herbalist, a masseur and an oxygen spa, was opened in 2006 and shuttered in 2013. It also considered expansion to Shanghai and Dubai but nothing has materialised. Nevertheless, Harrods has opened cafés under franchise agreements in Japan and Thailand as well as duty-free shops at Heathrow, Gatwick and Doha’s Hamad airport.

But these are side shows, relatively speaking. What is more interesting is the department store’s recent foray into specialty beauty retail with its H Beauty format. The UK is one of the few markets in the world in which Sephora hasn’t murdered the department store beauty floor and Harrods Knightsbridge is already the biggest seller of beauty products in the UK, with 9.3 percent market share. The three locations selected thus far, though, are lacking in inspiration. Will Harrods venture further down this road or will it, like Harvey Nichols’ Liverpool Beauty Bazaar, be a cul-de-sac?

Concept stores are all the rage, with their roots initially in fashion-forward merchandising exemplified by Dover Street Market and Colette. Dover Street Market also likes to throw in some curveballs in terms of store design, such as corrugated iron and plasterboard dividers, the use of reclaimed shipping containers to construct shop-in-shops and changing rooms made out of portaloos. This all creates huge amounts of hype as well as a cult following. Whether the approach is always profitable for either the store operator or brands is another question.

Galeries Lafayette threw its hat into this ring with the launch of a concept store on Champs Elysées in 2019 with mixed results. The store has been successful with Millennials — the average customer is just 31, younger than the typical online shopper in France — drawing them in with sleek design, elaborate pop-up installations and weekly events.

ADVERTISEMENT

Downtown duty-free made a brief comeback before international travel was shut down by the spread of Covid-19. The concept had become huge in Asia, notably South Korea, Hong Kong and Macau, but struggled to find its footing in Europe and North America. Nevertheless, DFS has opened two stunning locations in Europe: Venice’s Fondaco dei Tedeschi (2016) and Paris’ La Samaritaine (2021), the latter of which aims to go beyond the traditional duty-free format and draw in a fashionable local crowd so as to give it the cachet to attract international tourists.

Fighting online giants

Online multi-brand retailers such as Net-a-Porter, Farfetch, Yoox and even Amazon have dealt life-threatening wounds to the department store sector by offering the same breadth and depth of selection from the comfort of a customer’s armchair. The deployment of AI tools will likely up the ante for online players who will be able to identify and meet customer demand with ever-increasing speed and accuracy.

Department store groups have invested heavily in online, especially since the pandemic forced them to shut their doors, but they are playing a game of catch up. Selfridges.com was launched in 2010 with the main purpose of supporting the brick-and-mortar experience, for example by offering to book appointments at some of the store’s concessions (for example, Dior) which are still reluctant to sell online via the store.

The pandemic did change this dynamic somewhat and Selfridges saw an almost 50 percent increase in online sales in the year ended February 2021. The share of Selfridges customers who shopped online more than doubled from 19 percent to 45 percent in 2020, and the company expects this to stick at 32 percent for 2021, even with stores open. Assuming that Selfridges’ turnover will recover to roughly its 2019 levels (c. £850 million), that would represent around £270 million in e-commerce sales. By comparison, Farfetch’s gross merchandise value in 2020 was over $3 billion.

The challenges facing department store operators wishing to compete in the digital space are the reluctance of some luxury brands to explore this route to market with them, the significant investment in technology required to make their websites stand out and the logistical headache of international pricing and fulfilment. Harrods has taken the bold step of outsourcing its dotcom business to Farfetch, thereby sidestepping two of these challenges.

But ultimately experiential retail and best-in-class customer service are the ways to maintain an edge over e-commerce platforms. Selfridges has experiential retail in its DNA. The department store created a scandal in 1913 when it exhibited the wreckage from a failed attempt at a transatlantic flight on its rooftop. That spirit remains alive and kicking today, thanks in part to Vittorio Radice’s radical revamp of the department store in the 1990s (Radice stands to be reunited with Selfridges under the umbrella of Central Group/Sigma). Selfridges customers can have lunch, catch a movie, skateboard and even get married, as well as shop, shop, shop. The department store also has two personal shopping lounges, though this is no longer much of a differentiator vis-à-vis online players and their own VIP services.

Nordstrom has adopted a different strategy to fend off online competitors. The US department store group offers online shoppers the option to browse through products that they can pick up the same day from their local store. The Nordstrom Local programme, launched in 2017 has been met with some success and is being rolled out with the group betting that the inventory-less locations will draw customers in with the convenience of pick-ups, returns, alterations and other offerings, such as free return services to other online retailers. The group also launched a resale shop which not only allows customers to buy second-hand products but monetise their wardrobes, a service that is likely to have appeal to cash- and ethics-conscious Gen-Z’ers.

ADVERTISEMENT

Alive but at what cost?

The bottom line: department stores with a distinct point of view and unique offering are here to stay. Nevertheless, that comes with a steep price tag. Harrods forked out a reported £200 million on its Knightsbridge beauty hall. Selfridges spent $415 million on its new accessories hall; and it looks like a whole lot more money will be piled into Selfridges group by its new owners as evidenced by the Signa chairman’s statement that “together we will work with the world’s leading architects to sensitively reimagine the stores in each location, transforming these iconic destinations into sustainable, energy-efficient, modern spaces, whilst staying true to their architectural and cultural heritage.” Does anyone hear the sound of a ringing cash register?

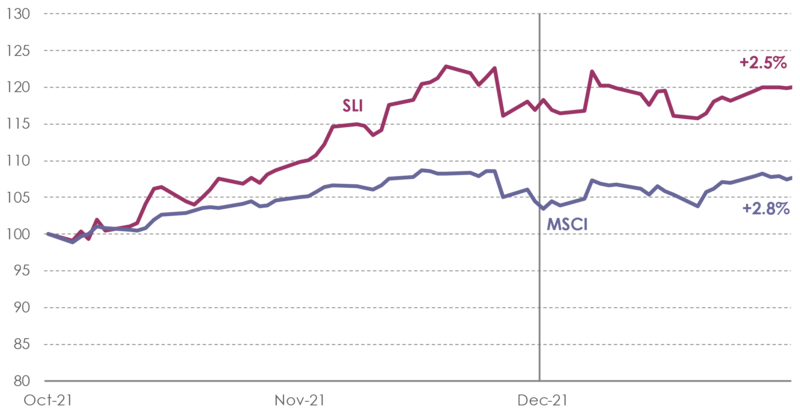

The Savigny Luxury Index (“SLI”) gained over 2.5 percent in December broadly in line with the MSCI’s 2.8 percent gain for the month.

Going up

Going down

What to watch

Digital streaming services are the new frontier in retail, a mixture of brand monetisation and awareness building. Rihanna’s Savage x Fenty shows on Amazon Prime break the internet; lifestyle brand and retailer Goop has a docu-series on Netflix and Pat McGrath Labs has recently announced a collaboration with Netflix hit show Bridgerton. Department stores such as Selfridges, Harrods and Berdgorf Goodman haven’t yet jumped on this bandwagon. How long until they do?

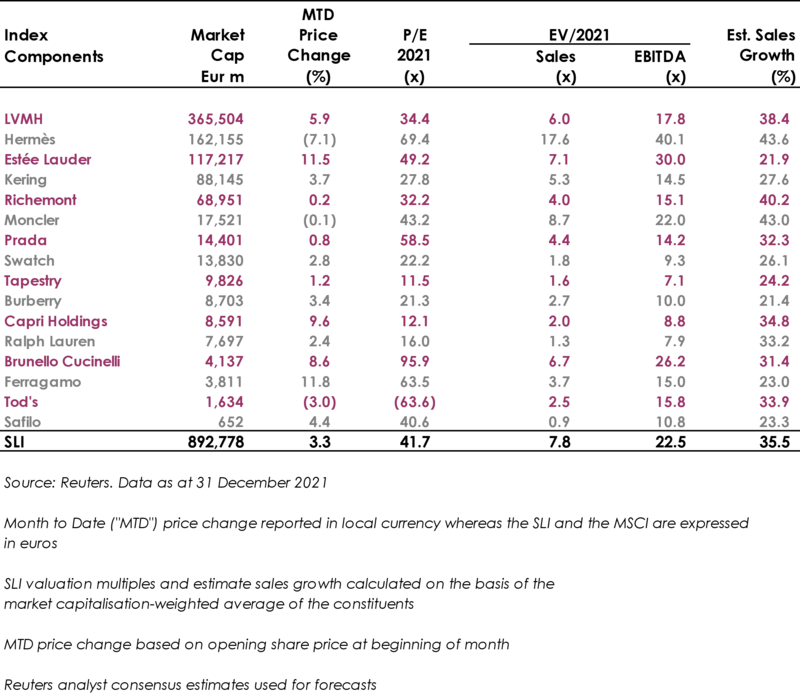

Sector valuation

Pierre Mallevays is a partner and co-head of merchant banking at Stanhope Capital Group.

Thailand’s Central Group has partnered with Austria’s Signa Holding to acquire Selfridges in one of the UK’s biggest retail deals in years.

Comme des Garçons’ chain of luxury bazaars reimagined multi-brand retail. Now, CEO Adrian Joffe is aiming to do it again with radical events platform 3537.

American luxury retail has changed, but customers are still hungry for the special feeling only an exceptional multi-brand store can offer. Can a crop of upstarts and a few savvy incumbents succeed where others have failed?

The former CFDA president sat down with BoF founder and editor-in-chief Imran Amed to discuss his remarkable life and career and how big business has changed the fashion industry.

Luxury brands need a broader pricing architecture that delivers meaningful value for all customers, writes Imran Amed.

Brands from Valentino to Prada and start-ups like Pulco Studios are vying to cash in on the racket sport’s aspirational aesthetic and affluent fanbase.

The fashion giant has been working with advisers to study possibilities for the Marc Jacobs brand after being approached by suitors.