The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

PARIS, France —As the coronavirus pandemic's long-term toll began to reveal itself, the fashion industry showed a rare semblance of solidarity. During one week in May, two groups of designers, executives and retailers published proposals to fix a broken system that relies on antiquated rules in order to buy, sell and market goods.

One, led by Belgian designer Dries Van Noten, urged the industry to say no to early-season discounting and move the delivery schedule back a few months, making warm-weather clothes available in warm-weather months, and cold-weather clothes in cold-weather months. Another, dubbed #rewiringfashion and facilitated by BoF's Imran Amed and Tim Blanks, took things further, calling for a shift of the entire fashion calendar, starting when clothes are presented to buyers, press and consumers and ending when they are put on discount.

The efforts gained widespread support, with more than 1,500 industry figures, from Proenza Schouler designers Jack McCollough and Lazaro Hernandez to Bergdorf Goodman’s Linda Fargo, signing the #rewiringfashion petition. But missing from the conversation were many of the most powerful brands in the world, including Prada, Hermès and Chanel, as well as those owned by multinational conglomerates LVMH and Kering.

When they first assembled, these independent groups did not invite the heavy hitters to join in their conversations, mostly because they're facing two very different realities. Many of luxury’s top players don’t need things to change so quickly. The current system, with all its faults, has worked well for them. They sell most of their goods directly to the consumer, which means they don’t have to go on discount if they don’t want to. They increasingly own — or at least control — their manufacturing, which means they can choose when to ramp up production or when to slow it down. They can stage a runway show any time of the year they’d like, and are able to put enough marketing dollars behind it to make it worthwhile. Their finances give them the freedom to do as they please.

ADVERTISEMENT

However, as conversations advance, the megalabels are announcing plans that so far align with the independents. Kering-owned Gucci recently said it would go "seasonless," scaling back to two fashion shows per year, while Saint Laurent — also owned by Kering — said that it would skip fashion week this fall, planning instead to show at a yet-to-be-determined time when it makes the most sense for both the brand and its customers. No LVMH brands have made announcements, but the group has recently joined in the discussions already underway.

The independent players know that if they really want things to change, especially when it comes to the fashion week calendar, they won't be able to do without the support of the strategic groups. In an industry in the midst of major consolidation, that's who holds the cards.

LVMH and Kering’s primary battleground is the market for personal luxury goods, worth €281 billion (about $311 billion at current exchange rates) in 2019, according to Bain & Company. A back-of-the-envelope calculation finds that about 40 percent of the market last year was controlled by five companies — LVMH, Kering, Richemont, Hermès and Chanel. To come to this number, BoF took the direct-to-consumer sales of each company and added them to an estimate of retail revenue from wholesale partnerships. The market share, in reality, is probably larger.

The two conglomerates came to dominate the category over the last three decades by snapping up dusty, family-run fashion and leather goods houses and transforming them into global brands backed by corporate infrastructure and large sums of capital. This allows them to control their own supply chains, recruit top talent, develop the most sophisticated marketing and advertising strategies and spend handsomely on prime release estate.

The Versace store in Galleria Vittorio Emanuele II | Photo: Getty Images

For instance, in the early days of 2020, LVMH made headlines for offering to pay record rents for new Dior and Fendi stores in Milan’s historic Galleria Vittorio Emanuele II shopping arcade. After winning a public auction, Dior will pay €5 million (about $5.5 million) a year for its space, while Fendi will pay €2.4 million (about $2.6 million). The current tenants, smaller Italian rivals Versace and Armani — two global fashion brands with roots in the city — simply could not compete with these bids.

Of course, those bids were placed before the outbreak of a novel coronavirus became a pandemic, killing hundreds of thousands of people, leaving millions others unemployed and forcing the global economy into a severe recession. Today, in the age of Covid-19, the LVMH and Kering empires are being put to a great test. The luxury sector is forecasted to contract by up to 39 percent this year, according to BoF and McKinsey & Company's Coronavirus Update to The State of Fashion 2020. Retail stores across the world were shut down by government-enforced lockdowns and, while consumers in most places were able to shop online, many simply didn't want to — or could no longer afford non-discretionary purchases.

That lack of consumption has already hit the industry hard. Fashion brands and retailers encumbered by debt are closing. Factories are panicking, waiting on payments while sitting on goods that were produced pre-crisis. While China's re-opening in early April has provided a glimmer of hope, the outlook remains uncertain, with consumer spending in the country down 7.5 percent from a year earlier. Chinese consumers are by far the biggest driver of growth for luxury, but much of their money is spent during overseas travel, which has effectively stopped. The tourism industry is projecting a recovery timeline of three to five years, and shopping habits — including Chinese spending money abroad while travelling — may never return to normal. Morgan Stanley projects that LVMH's organic sales will decrease by 49 percent in the second quarter of this year, versus 17 percent in the first quarter, with annual sales down 18 percent and EBIT (earnings before interest and taxes) down 22 percent.

ADVERTISEMENT

A boarded up Dior in Paris | Photo: Daniel Korkhov

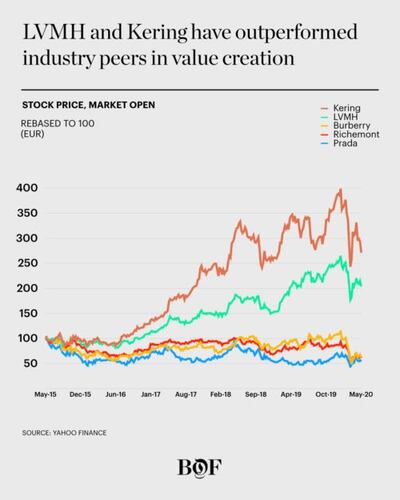

As a result, stock prices have taken a hit. As of May 25, LVMH’s share price was down 13 percent from the beginning of the year, while Kering’s was down 26 percent. The CAC-40 Index, which includes 40 of the most important stocks traded on the Euronext Paris, was down about 24 percent year-to-date.

The strategic groups' relative resilience has made analysts confident in the long-term health of both businesses. In luxury, like other industries, only the strong — those with the tightest production lines, the biggest networks and the most cash — will endure. And if any companies are going to emerge from the coronavirus pandemic more powerful, it’s LVMH and Kering.

Luxury is Europe's big tech.

Just as the FAANG companies (Facebook, Amazon, Apple, Netflix and Google) have come to dominate not only their own industry — technology — but also culture and commerce, LVMH and Kering have done something similar in luxury. “Luxury is Europe’s big tech,” said Scott Galloway, a professor of marketing at New York University’s Stern School of Business. “Consolidation like that is very hard to reverse.”

Before any of this happened, the luxury fashion industry was already consolidating around a handful of key players, including independent operators Hermès and Chanel, as well as strategic groups including Switzerland’s Richemont — which owns Cartier and Chloé — Italy’s OTB Group, owner of Diesel, Maison Margiela and Marni, and newer US-based firm Capri Holdings, which controls Jimmy Choo, Versace and Michael Kors. But none is as mighty as the two dominant groups.

“LVMH and Kering have built a competitive advantage that will just increase over time,” said Mario Ortelli, managing partner at Ortelli & Co., a strategic advisory. “It’s very difficult for anyone else to catch up.”

The Genesis of Modern Luxury

The rise of LVMH and Kering tells a fairly neat-and-compact story of the formation of the modern luxury industry. Owning and displaying luxury goods has long been a way to communicate social status, but 20 years ago, it just wasn’t as common to possess a Louis Vuitton bag or a Gucci watch if you were middle class. The concept of masstige — or shiny, luxury-branded products that a large constituency of consumers can afford, or at least feel comfortable charging to their credit card — was only in its infancy.

ADVERTISEMENT

With the revival of old houses, that began to change. While the Chanel flap bag was invented in 1929, it didn't go mass until Creative Director Karl Lagerfeld embedded an interlocking CC into the closure in the 1980s. In 1994, the house of Dior introduced a quilted, top-handled rival to Chanel's flap, and called it the Lady. But it was the introduction of Fendi's baguette in 1997 that marked a turning point. Created by Silvia Venturini Fendi, who was inspired by a skinny bread loaf, the clutch became a status symbol in popular culture, imortalised in the HBO television series "Sex and the City."

In the early days of these house revivals, companies relied on new interest from European and American consumers, as well as the Japanese market, which became important to luxury from the 1970s when the country's economy experienced tremendous growth.

The Arnault family, which controls LVMH and its 70-strong brand portfolio, didn't start in luxury, but in real estate. Its construction business shifted into the buying and selling of property in 1976. But by 1984, patriarch Bernard Arnault, the current Chairman and Chief Executive of LVMH, had bought the company that owned both Christian Dior and Le Bon Marché. Arnault didn't create LVMH — Alain Chevalier, chief executive of Moët Hennessy, and Henry Racamier, president of Louis Vuitton did — but he gained control of the business in 1989 after buying up shares over the course of two years. It would take another decade for Arnault's playbook for reviving brands to coalesce, but he certainly took more than a few cues from Chanel, which was already on its way to building a global powerhouse.

Under Lagerfeld, Chanel devised a product pyramid still used by luxury brands today, one that takes brand heritage — which helps to earn the consumer's trust — and melds it with relevance, which helps create desirability. At the top of the pyramid is couture, followed by ready-to-wear, then shoes and handbags, then sunglasses and other entry-price accessories, then finally fragrance and makeup. (In more recent years, streetwear — sneakers and t-shirts — has also been layered in.)

Couture sold the dream, as French fashion executives like to say, while the accessories, fragrance and makeup generated the cash.

Marc Jacobs at a Louis Vuitton runway show in 2004 | Photo: Getty

In the mid-1990s, Arnault began pairing his heritage brands with young, lauded talents, fueling a cult around his creators: John Galliano at Givenchy (1995) and then Dior (1996), Alexander McQueen at Givenchy (1996), and Marc Jacobs at Louis Vuitton (1997). He did away with the cheap licensing deals done in the 1970s when the bottom fell out of the couture business and started building up these labels again from scratch, working to create a myth and product hierarchy as strong as Chanel's. (In the early 2000s, he would also buy Italian furrier Fendi, where Karl Lagerfeld had been creative director for more than 50 years.)

At the same time, a rival was forming in Italy. The Gucci Group, brainchild of business executive Domenico De Sole and his creative partner, Tom Ford, took a slightly different approach, starting with Gucci and adding a mix of heritage and emerging houses, including Yves Saint Laurent — called "fashion's biggest prize" by journalist Suzy Menkes — in 1999, Alexander McQueen in 2000 (who by that time had exited LVMH) and Stella McCartney in 2001.

Two Rival Groups

In the late 1990s and early 2000s, LVMH and Kering — then known as PPR — tussled for several years over the acquisition of the Gucci Group. PPR was founded by François Pinault, a French businessman who started in the lumber trade but moved into retail by the late 1980s, buying up French department store Printemps, electronics retailer FNAC and others. The company increased its stake in Gucci Group to 42 percent in 1999, with the intention of fending off a "creeping takeover" by LVMH. (Over the years, Arnault has tried similar tactics with Hermès — to no avail — and won LVMH this way in the first place.) At one point, De Sole wanted to make a deal with LVMH, but Arnault rejected his proposal.

This was no quiet battle. ("One of the most bitter fights in corporate history," wrote Suzanne Kapner in the New York Times.") PPR played the white knight by sweeping in and making a deal that was much better for the Gucci Group than what LVMH was offering. De Sole and Ford would be given the opportunity to operate somewhat independently from the rest of the group, while a partnership with LVMH could mean the dissolution of their current operational structure.

Domenico de Sole talks with Francois Pinault during YSL show in 2003 | Photo: Getty

PPR won Gucci Group for a little under $9 billion, though Ford and De Sole exited in 2004 after it fully acquired the business. But there’s no denying that Arnault’s decision to reject De Sole’s offer was a turning point for the luxury industry, paving the way for two rival groups, even if one was 20 years ahead of the other.

"Rather than putting an end to the feud between Mr. Pinault and Mr. Arnault, the deal that was signed at 3 a.m. today in Paris is merely the closing of one chapter in what analysts predict will be a long and juicy tale," the Times wrote. "In addition to competing for acquisitions and design talent in the world of high fashion, the two men will still face each other in other industries, including telecommunications, publishing, art and wine."

What LVMH and PPR now had were a stable of luxury brands, constructed around cash cows Louis Vuitton and Gucci, respectively. They were best positioned to take advantage of the opportunity ahead.

Big Luxury Takes Flight

In the aftermath of the 2008 financial crisis, the fashion industry underwent its biggest transformation yet. As the gap between the rich and poor increased — in 2020, 70 percent of the global population lives in countries where the wealth divide is widening — fashion brands at the high end (luxury) and low (discount and fast fashion) continuously won out over the once-dominant middle market.

Suddenly, it wasn’t just older, wealthier people buying luxury goods, but young consumers, too, whose post-recession spending habits were focused more on personal extravagances than ever before. While Generation X scoffed at the transformation of counter-culture Baby Boomers from hippies to money-driven conservatives in the 1980s, deeming it deeply uncool, Millennials and Generation Z embraced consumerism without irony. They often prioritised shopping for material goods over investing in items that were once considered the building blocks of an optimal life. Rent the house instead of taking out a mortgage, call the Uber instead of owning a car, buy the Gucci loafers.

Queue outside a Louis Vuitton store in Turkey, 2018 | Photo: Getty

That shift in priorities in the West, combined with the rapid acceleration of new wealth in China, has afforded luxury brands the ability to grow at lightning speed. Last year, Chinese consumers accounted for 35 percent of the market overall and 90 percent of global market growth, according to Bain. (By 2025, Chinese consumers will account for half of spending in the category.) Other growth markets — in particular, the Middle East, Korea, Russia, Brazil and India — have also played an integral role.

In 2019, Kering-owned Gucci generated €9.6 billion (about $10.5 billion) in sales, up 317 percent from €2.3 billion (about $2.5 billion) in 2009, when the group was still called PPR. While Kering has pruned its portfolio over the past decade to focus solely on personal luxury goods — fashion, accessories and jewellery — its share price increased to more than €561.60 (about $621) at the end of 2019, up 836 percent from €59.99 (about $66) in December 2009.

LVMH, which is more than three times the size of Kering, has broadened its areas of interest, buying up companies that deal in hospitality and hard luxury, including Belmond hotels and Italian jeweller Bulgari, among others. In 2019, it generated €53.7 billion (about $58.9 billion) in sales, up 214 percent from €17.1 billion (about $18.8 billion) a decade earlier. With several major acquisitions, including the integration of Dior into the main business in 2017, its share value has also increased dramatically to €404.50 (about $447) at the end of 2019, up 540 percent from 63.13 (about $70) in 2009.

Much like their customers, luxury's rich have only gotten richer, while it's harder than ever for less-well-off competitors to succeed. In 2019, 97 percent of economic profits for public fashion companies were earned by just 20 corporations — including LVMH, Kering, Hermès and Richemont — according to McKinsey and BoF's State of Fashion 2020 report.

The Little Victims

Consolidation is natural. It makes industries more efficient. The luxury industry, with its handful of major players, is in the third stage — or the "focus" segment — of the process, according to a 2002 Harvard Business Review article on the theory of the "consolidation curve," written by three executives from consulting firm A.T. Kearney. "This is a period of megadeals and large-scale consolidation plays," they said. "The goal is to emerge as one of a small number of global industry powerhouses."

Kering and LVMH, first movers in personal luxury goods, have used their profits to strengthen their positions.

As they’ve grown in scale, LVMH, Kering and Richemont — along with fiercely independent, family-controlled players Chanel and Hermès — have worked to gain as much control as possible over their businesses, building vertically integrated operations by buying up factories and opening new ones, but also taking more of their sales direct to customers, controlling the best real estate in high-end malls and on major retail streets. Through partnerships with top fashion and business universities, as well as competitions like the LVMH Prize, they have also built pipelines that allow them to recruit and retain top creative and executive talent.

Chanel and Hermès have managed to maintain their position versus LVMH and Kering because of the strength of their brands and their robust operations. Most importantly, they began scaling long before the two strategic groups were even formed and remain large enough to fend off unwanted interest from potential acquirers. They also both started buying suppliers and factories years ago, and Chanel — the largest luxury brand in terms of volume, with more than $11 billion in annual sales — has always directly owned its beauty and fragrance business, the biggest driver of topline revenue. Additionally, they have the backing of families that seem, for now, wholeheartedly dedicated to remaining independent.

But for most other brands, LVMH and Kering have made operating solo incredibly difficult.

Consider the case of Stella McCartney, who learned the hard way how difficult it is to be independent when she separated from Kering, her longtime financial partner, in 2018. The decision was hers, but with sales under €300 million (about $329 million), the designer's nearly 20-year-old brand was never a significant source of revenue for the group.

LVMH board director Delphine Arnault with Stella McCartney in 2019 | Photo: Getty

Less than a year after the split, she found herself in the arms of LVMH. Arnault certainly didn't need McCartney to grow his business. But he could benefit from her knowhow and authority when it came to the sustainability conversation, a burgeoning battleground in which Kering was seen to be ahead of the curve. McCartney's motivations were pragmatic. She needed the support that comes with being in a group — managing global distribution, IT, human resources and other functions — to seriously compete, and would also have the ears of the most powerful man in fashion when it comes to driving the sustainability conversation.

Antoine Arnault, the second of Bernard Arnault's children from his first marriage, insists that there is room for independent players, and that LVMH fosters their development by recruiting young designers — who sometimes go on to launch their own brands — or by sponsoring young upstarts through the LVMH Prize. Or, as with the case of Jonathan Anderson and, before him, Marc Jacobs, funding a small brand so that its designer can front one of the company's marquee brands.

If you only have three big TV channels, isn't it going to be a little boring?

“When we look at the industry as a whole, we need those younger, smaller brands to exist, to create interest into the market,” Antoine Arnault said. “If you only have three big TV channels, isn’t it going to be a little boring?”

“We buy smaller brands, we don’t only acquire brands such as Tiffany or Belmond,” he added, mentioning the McCartney partnership. “Everyone can play his part in this big game… clearly we are playing our part well.”

Kering Chief Financial Officer Jean-Marc Duplaix echoed that sentiment. “There is still room for small brands or emerging brands, but these brands have to accept that they need to grow and develop quite slowly,” he said. “They should be focused on certain categories, as the cost to expand is very high.” However, he also noted smaller brands can be a distraction for a group: “I’m not sure that the recipe can really work.”

Kering has backed away from these sorts of investments, selling its majority stake in Christopher Kane back to the designer in 2018 and instead using Artemis, the family's personal investment arm, to make smaller bets on rising labels like Giambattista Valli. (However, Kering still owns a significant minority interest in American brand Joseph Altuzarra.)

As McCartney learned, if you do want to build a global luxury fashion business, doing so without the help of one of these groups is now practically impossible. Even other groups are struggling to compete against such colossal operations.

The Big Victims

Source: BoF

It's not just independently operated firms that are threatened by LVMH and Kering. Richemont SA, best known as the market leader in hard luxury as the owner of Cartier and Van Cleef & Arpels, is the third member of luxury's Big Three. But the cash-rich group has had difficulty keeping up with its rivals. For one, it has never been able to crack the fashion category, lacking the necessary knowledge on how to make, market and distribute soft goods. Now, its collection of fashion brands — including trend-sensitive Chloé and connoisseur-favourite Alaïa — are often pushed aside on retail floors by their stronger, more aggressive competitors despite their tremendous potential. (It's telling that Chloé was the first major label to join Van Noten's recent efforts to fight discounting.) Other major brands, including Prada, Ralph Lauren and Burberry, face similar challenges. As does Mayhoola, the Qatari-backed investment fund that owns Balmain and Valentino.

More recently, Richemont has struggled to maintain its position as the leading seller of fine jewellery, as both LVMH and Kering have made significant inroads in the category. LVMH's expected $16.2 billion acquisition of Tiffany, combined with its $5.2 billion majority stake in Bulgari in 2011, has positioned it as a real competitor in the space.

To maintain a competitive advantage, Richemont has invested in multi-brand e-commerce — where neither of its competitors have a foothold — buying Yoox Net-a-Porter Group (YNAP) in 2018 for about $3.3 billion, although that bet has yet to pay off. In the first half of its most recent fiscal year, net profit was down 61 percent in the period to €869 million (about $953 million). LMVH's own attempts at developing multi-brand e-commerce — eLuxury in 2000 and 24 Sèvres (24s) in 2017 — were unsuccessful. eLuxury shuttered in 2009, while Arnault has downplayed the group's efforts around 24s, the digital version of its famous Left Bank department store Le Bon Marché.

“We haven’t found a way to make it profitable...it is almost insignificant to us,” he said in January 2020, adding that he is “somewhat sceptical of the category overall.”

“All of them are losing money,” he said, regarding existing players including YNAP and Farfetch. “The bigger they are, the more money they lose.”

Kering, which exited a strategic partnership with YNAP in 2018, is focused on further developing its individual brand sites, which still make up a small percentage of overall sales. (Gucci’s e-commerce has operated independently since 2002.)

Post-pandemic, it seems that it will be even more challenging for the likes of Richemont to maintain their positioning within the luxury fashion ecosystem. "In the aftermath of a crisis, resilient players can outperform rivals," according to BoF's recent update to The State of Fashion 2020 report. "Power can be consolidated as previously held market share is freed up once competitors fall away."

So, then there were two.

A Winning Playbook

There are many reasons that the industry has consolidated around LVMH and Kering. One of the most important is that they are both vigilant brand stewards and believe in strong creative leadership alongside strong executive leadership. Over the years, LVMH’s approach to brand building has remained virtually the same. Take a name — one with a history — and build on it with exciting fashion, fresh cosmetics and trendy accessories until it has achieved fashion legitimacy. Sometimes that happens more quickly than with others.

“From the beginning, Mr. Arnault was more focused,” Ortelli said.

Antoine Arnault said that while there is no exact recipe to his father’s success, there are certain fundamentals. “The first one is to respect and worship the history and core values of a brand,” he said. “Once you really understand, once you’ve dug into the heritage and archives and know it inside out, you must assemble the best teams to combine performance and creativity.”

Kering's approach is slightly different, especially with the transition of power in 2005 from founder François Pinault to his son, current Chairman and Chief Executive François-Henri Pinault, who has spent the last 15 years recalibrating the company's portfolio to focus solely on fashion and hard luxury, with a tight group of labels that almost all have the potential to become megabrands generating well above $1 billion a year.

“At the beginning, PPR was more like private equity: it was about finding opportunities in different sectors and investing in it,” Ortelli said. “Then, luxury became its expertise.”

While LVMH has a heritage-first approach —its most popular brand, Louis Vuitton, was originally a luggage maker — Kering is more exposed to fashion labels like Yves Saint Laurent and Balenciaga. Some argue this is a riskier prospect that’s more susceptible to the ebb and flow of trends.

“LVMH is overweight on heritage brands; Kering is overweight on fashion brands,” Ortelli said. “Heritage is constant, with less volatility. In fashion, you’ve got a more volatile road.”

There are exceptions to this rule: LVMH-owned Celine is not obviously trading on any fixed core heritage; just look at the stark difference between the collections designed by former creative director Phoebe Philo and current creative, artistic and image director Hedi Slimane. Neither has Givenchy in its multiple reinventions, despite its long history. Conversely, while Gucci may be under the spell of Alessandro Michele, its bestsellers — loafers, logo belts — are classics that have been available to purchase for decades in one iteration or another.

Kering does not agree with the assessment that its houses are more trend-driven.

Gucci Cruise 2020 runway | Photo: Getty

"The brand is symbols, icons — it's never a style," Pinault told BoF in a 2018 interview. "The style is the interpretation of something and if you think that the style of the brand has to be respected, you never move forward."

Duplaix said Kering’s formula requires the creative director to evolve the brand’s style without losing sight of its heritage.

“As a corporation, we ensure there is a framework, but it’s not a science,” he said. “We start with product and creativity, to make sure there is a clear definition of the brand.

One approach isn’t necessarily better than the other. They are fundamentally grounded in the same thing: selling expensive, fashionable handbags and accessories to Chinese consumers through smart storytelling. But they each have their strengths and weaknesses. LVMH has a diverse portfolio of brands — in several categories, including travel and beauty — which means it does not need to pressure any one brand to outperform — while Kering’s ability to identify and amplify creative talent has been unmatched in recent years.

Dior Men by Kim Jones | Photo: Getty

From the elevation of Michele at Gucci and, more recently, the matchups of Demna Gvasalia at Balenciaga and Daniel Lee at Bottega Veneta, Kering has made genuine cultural waves. While LVMH has done well to market its leading brands by installing Virgil Abloh at Louis Vuitton and Kim Jones at Dior, the critical and commercial success of their collections, while important, is not the dominant factor in the success of those houses.

The group's other recent attempt at tapping the zeitgeist, a fashion venture with pop star Rihanna, has yet to take off. Neither has Slimane's Celine reboot. In fact, neither group has much ability to create new brands from scratch, in part due to the inherently high capital requirements and risk involved. Instead, they've both achieved a dominant position by snapping up properties that are already well known and ensuring the right management and creative teams are in place.

There's also a difference in attitude at the groups. Kering has built a more casual corporate culture that avows transparency and a start-up mindset — with near-continual press releases about the inner workings of the company, from environmental policies to employee wellbeing — that is, ultimately, driven by the personality of François-Henri Pinault.

LVMH, by contrast, is almost monarchical. However, that's changing as the new generation of Arnaults take on leadership roles: Antoine Arnault, chief executive of Berluti and chairman of Loro Piana, is also the group's head of image, communication and environment, as well as a member of the LVMH board of directors. Then there's Delphine Arnault, director and executive vice president of Louis Vuitton, who is also a board director, Alexandre Arnault, chief executive of Rimowa and Frédéric Arnault, strategy and digital director for Tag Heuer. (The youngest heir, Jean, is still studying.)

The Black Swan

By the end of 2019, the industry’s two superpowers seemed, in many ways, invincible, making it harder and harder for others to succeed alone, or even within a less well-positioned group.

The coronavirus outbreak, in some ways, has underscored their enviable positions. Despite the crisis, both groups have the ability to continue to pay employees, to control inventory and to provide support by producing, or at least paying for, medical supplies and new hospital wards.

The main focus is not how they will survive the crisis, but which companies may make for opportunistic acquisitions, as once-independent businesses determined to go it on their own grow tired of the fight.

Several Italian firms, including Moncler and Salvatore Ferregamo, are often surfaced by analysts and bankers as potential targets.

Prada store in Paris | Photo: Daniel Korkhov

In recent months, speculation that Prada, which has been around longer than Louis Vuitton or Chanel, would be acquired by Kering, has continued to mount. And yet Prada — which recruited Raf Simons to be mastermind Miuccia Prada's co-creative director this year — has denied it's for sale. (Lorenzo Bertelli, the son of Prada and her husband, Co-Chief Executive Patrizio Bertelli, is being groomed to take over.) Kering declined to comment on Prada. But the possibility remains, and would be a smart deal for both companies, said Elsa Berry, managing director and founder of Vendôme Global Partners, a New York-based strategic mergers and acquisitions advisory firm.

“I think many, many independent brands will realise after this global crisis that it is more and more challenging to remain so,” she said. “Unlike Moncler, where the valuation is high and future growth may be less significant and certainly where Kering’s knowhow will be less needed and less relevant, Prada would be an ideal fit for both sides. Kering can patiently grow and add value, and for Prada shareholders, they get, with Kering, a solid track record.”

However unlikely, a Prada acquisition would be a boon. Over the years, Kering has made deals in other categories with varying success — including the acquisition of Puma and the purchase of Bocheron — but not in the group's core category, fashion. Pinault has said he is looking for a globally recognised, sizable brand that will not directly compete with any of the brands currently in the portfolio. (Versace, once a hot prospect, was acquired by Capri in 2018 for more than $2 billion, a price Kering believed to be too high.)

LVMH, too, is focused on making big acquisitions, like the Tiffany deal, which was decades in the making and is expected to take place even with pandemic-related setbacks. While LVMH seems dedicated to continue to develop smaller brands and new brands — its relaunch of Patou, and the FENTY by Rihanna fashion brand — its track record in that department remains unproven. Gone are the days of scooping up a $200-million-revenue business in the hopes of scaling it quickly to $1 billion. Now, they're looking for $1 billion companies they can scale to $10 billion.

The Future

The pandemic may very well bring new challenges to the luxury sector at large, but particularly to those who dominate it, and who might be reluctant to change when the rest of the industry seems to be hungry for a reset. For every Woolworth, there’s a Walmart, and for every Walmart, there’s an Amazon.

LVMH and Kering are both extremely reliant on Chinese customers — and that dependency is likely to increase as China’s economy continues to grow, albeit much more slowly, with many analysts estimating that it will be the least affected region in the ensuing economic crisis.

While that’s not necessarily a bad thing — even as spending slows in the region — it may become harder to win over those consumers as their consumption habits change, the market rapidly matures and shoppers start to care less about certain old-fashioned status symbols that have been adopted by the masses. They will begin to obsess less over failsafe blockbuster brands and more over new prospects. China may even begin to create its own global luxury labels, something it has failed at in the past.

The luxury industry is also far too reliant on driving up prices of individual items to increase profits. (Today, handbags often cost well over $3,000 a piece. Shoes, $1,000 a pair.) Rising prices of goods were fine when the economy was minting new millionaires, and billionaires, at a steady pace. (China added 182 billionaires over the year ending January 2020, according to the Hurun Global Rich List.)

But now, as the coronavirus has wiped out trillions of dollars in wealth, priorities — and consumer behaviour — may change in the medium term. What makes a handbag, or a pair of sneakers, worth it? As top brands including Chanel and Louis Vuitton begin instituting price increases in order to make up for lagging lockdown-era sales — inspiring consumers to queue up to buy the products before the hikes were put in place — the limit is going to be tested.

Image by Jan-Nico Meyer for BoF

One looming threat is luxury's lack of agency over its own secondary market. Consumers are already buying luxury products secondhand from the likes of The RealReal and Vestiaire Collective, and even renting them from US-based service Rent the Runway, showing that ownership is less important to the current generation of would-be luxury shoppers. There is an argument that LVMH and Kering, which tend to take a wait-and-see approach to new models before trying them out themselves, should already own this stage of the product lifecycle.

And while consumers will always find ways to express themselves through fashion, the specifics will change. They may prefer customised, made-to-order products. Or new categories: streetwear instead of gowns and protective face masks instead of shoes. Or they may simply choose to buy fewer things. High fashion is already fairly homogenised, and many argue it will only become more boring if just a few companies are producing just about everything.

In order for these giants to continue to dominate this next wave of consolidation, they will need to react quickly to the changes brought on by the pandemic, or risk the disruption they’ve managed to stave off thus far. For instance, LVMH is only now putting proper focus on e-commerce, a channel that will account for 30 percent of sales of personal luxury goods by 2025, according to Bain. (And that’s not considering the amount of purchasing done in-store that begins online.)

Perhaps most importantly, both LVMH and Kering’s models are predicated on the idea that wealthy people will continue consuming at a rapid pace. “It is easy to get carried away during a tragedy,” Bernstein analyst Luca Solca wrote in a recent note. “The legitimate aspiration to social elevation, being better off and having more, will persevere.” And yet, “On the back of the sharp recession to come... we do expect consumers will become more conservative,” Solca added.

This battle is far from over.

Disclosure: LVMH is part of a group of investors who, together, hold a minority interest in The Business of Fashion. All investors have signed shareholders’ documentation guaranteeing BoF’s complete editorial independence.

Additional Reading:

[ For Luxury, an Acceleration of the InevitableOpens in new window ]

[ Why Luxury Came to the RescueOpens in new window ]

[ At Kering and LVMH, Corporate Branding Goes Beyond the LogoOpens in new window ]

The Swiss watch sector’s slide appears to be more pronounced than the wider luxury slowdown, but industry insiders and analysts urge perspective.

The LVMH-linked firm is betting its $545 million stake in the Italian shoemaker will yield the double-digit returns private equity typically seeks.

The Coach owner’s results will provide another opportunity to stick up for its acquisition of rival Capri. And the Met Gala will do its best to ignore the TikTok ban and labour strife at Conde Nast.

The former CFDA president sat down with BoF founder and editor-in-chief Imran Amed to discuss his remarkable life and career and how big business has changed the fashion industry.