The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

This article first appeared in the special edition of The State of Fashion: Watches and Jewellery, co-published by The Business of Fashion and McKinsey & Company. To learn more and download a copy of the report, click here.

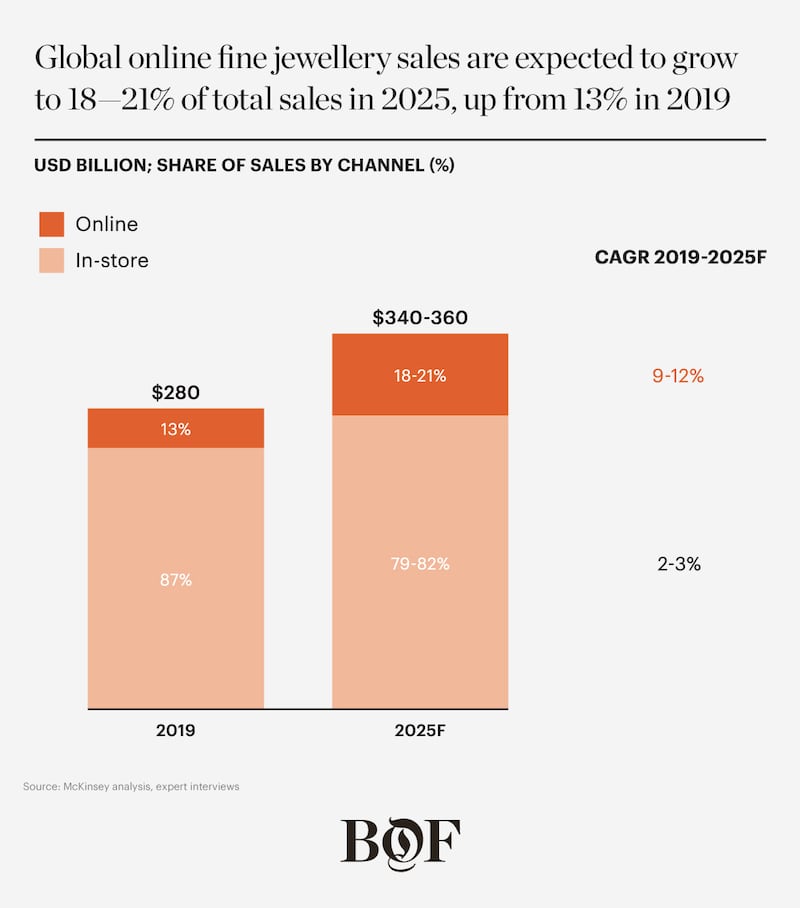

Fine jewellery and e-commerce are not the most natural pairing. The enduring appeal of face-to-face interactions in the digital era can be explained by several factors. Not only is the buying experience inherently emotional and the price significant, but fine jewellery purchases also often involve consultation, with fitting and confidence in the purchase frequently requiring professional, hands-on assistance. Fine jewellery has therefore been slow to move to digital, with the industry generating just 13 percent of its revenue online in 2019.

To make a break for digital, fine jewellery needed a catalyst, which materialised in 2020 with the global pandemic. As physical stores closed, fine jewellery consumers were forced to switch to online channels — and brands and retailers around the world had to quickly adapt, even in markets where security concerns are a high priority among luxury consumers. “People in Brazil, contrary to some in the United States, were very reluctant to buy jewellery through e-commerce [at first, but] they are not afraid anymore,” said Roberto Stern, president of Rio de Janeiro-based jeweller HStern. “Having clients learn to trust online sales was a big game-changer.”

As a sign of growing comfort with digital purchases, the US and European (including UK) markets saw a 57 percent rise in the number of fine jewellery pieces ordered online in 2020 compared to 2019, in addition to a 35 percent increase in the average unit value, according to exclusive Adobe Analytics data. To be sure, customer behaviours will settle post-pandemic, but the comfort baseline for online shopping for fine jewellery has been fundamentally reset. Over the next five years, online sales of fine jewellery are expected to grow at a compound annual growth rate (CAGR) of 9 to 12 percent, which is three times that of the overall fine jewellery industry.

ADVERTISEMENT

In response, brands, retailers and marketplaces are bulking up their online inventories, many with items and price points previously reserved for physical stores. Tiffany & Co customers, for example, can buy jewellery worth more than half a million dollars directly on its website. Online luxury marketplaces are following suit: 1stDibs lists jewellery priced at seven figures, of which one of the most expensive items is a 23-carat flawless emerald cut diamond ring by Harry Winston, selling for $4.45 million. As brands extend their online assortments, some are complementing high- resolution photos with augmented reality try-on and virtual appointments that enhance the online experience and serve practical customer needs.

With the increased comfort of purchasing big-ticket jewellery items online come opportunities to leverage social media and other digital platforms such as livestreaming. Though the verdict remains out for the channel’s efficacy for fine jewellery sales across many territories, it is gaining traction in China and other Asian markets. Cartier hosted its first jewellery livestreaming show on Taobao Live during Alibaba’s 11.11 shopping festival last year, featuring more than 400 watches and jewellery items and including a necklace valued at $28.3 million. The opportunity also spans beyond established jewellery brands. Social media has dramatically levelled the playing field, allowing younger challenger brands to disrupt the marketplace with their fluency in speaking to younger generations on social channels.

In light of these shifting dynamics, the future for fine jewellery online looks bright. McKinsey’s analysis expects the market to double between 2019 and 2025, with online reaching 18 to 21 percent of global fine jewellery sales and amounting to $60 to $80 billion in annual turnover. We see the growth impacting branded and unbranded players differently. For instance, brands selling directly online will be the clear winners, in large part driven by consumers’ preferences for buying directly from brands, with data from Agility showing that upwards of 60 percent of affluent consumers will turn to a brand’s own website for their purchase. Online platforms distributing branded fine jewellery, including both multi-brand e-tailers like Net-a-Porter and marketplaces like The RealReal, will benefit from the tailwinds, too.

Whatever their position in the market, time is of the essence if players are to claim a share of online sales growth. While larger players have the benefit of size and resources, it is likely that they will be overtaken by more nimble players with lower barriers to entry if they do not act fast.

The economics can be attractive for brands and retailers that decisively take action to boost their direct online sales. The direct-to-consumer (DTC) model can offer advantages such as a higher gross margin (sometimes even double), the ability to offer a lower price point to consumers, increased opportunities for cross-selling and up-selling, and the ability to own the customer relationship and drive repeat purchases.

However, if not properly managed, DTC costs can balloon, with increases felt in shipping, logistics and returns. Not all brands have found a sustainable equilibrium — for instance, in its 2020 annual report, Pandora highlighted a higher share of online sales as one of the elements impacting its margins.

The model also comes with increased expectations around transparency from online consumers. Unlike brick-and-mortar retail, online offers the ability to easily compare prices for similar items across sites. This is especially true for diamonds, where attributes of the 4Cs — colour, cut, clarity and carat — used to assess quality and therefore value, can be compared well enough for each gem. It will therefore be imperative for jewellers to compete on the basis of design and brand equity. As such, companies that have let creativity take a back seat will see their margin come under pressure. Others will embrace digital transparency and use it as an essential component of their value proposition. Online jewellery retailer Blue Nile, for instance, has made sharing information about the 4Cs — and being transparent about how this influences price — central to its brand, providing a transparent lens on a previously hard-to-quantify purchase.

While fine jewellery’s opportunity online is clear, what is less certain is how business leaders will create digital experiences that live up to the enchanting experiences for which physical fine jewellery stores are known. “It’s about the magic,” said Shaun Leane, founder of the UK-based jewellery brand of the same name, renowned for collaborations with the likes of Boucheron and Alexander McQueen. “That’s the world of jewellery and that’s what the consumer wants to see, feel [and] experience. They want to be buying a part of that.”

ADVERTISEMENT

Executives should consider the following actions when developing their own “magic” online:

Anchor ‘Magic’ in Use Cases

To start, companies will need to define the role of each digital channel and clearly articulate the use cases, or needs, that the channel should address for both the consumer and the business. With clearly defined use cases, jewellers can then better determine what type of “magic” is needed to deliver, or over-deliver, for the customer. Winners will master capturing the emotional dimension of the purchase and will elevate the experience beyond that of buying everyday items online. Some companies are using virtual reality apps and videos, alongside live events, to boost the sense of connection. For instance, Bulgari has developed a special app for key customers that enables them to discover the brand’s new collection and try the pieces on through augmented reality. Players should, however, be sure that the “magical” touches are linked to clear use cases and be wary of investing in gimmicks.

Leverage Store Networks

The rise of digital does not diminish the importance of physical store footprints. Among many roles, stores have historically acted as the crown jewel of brand experience, and they will continue to do so in the future. Jewellers with an existing store network should draw on their brick-and-mortar sales expertise to inform the online experience and leverage their resources across both channels. This could mean making their in-store sales force available for advice to shoppers both online and off, with staff available to try on jewellery and share via video with clients. Courbet’s virtual shopping experience, for example, leverages personal appointments with sales reps, including product recommendations and staff try-ons, which blends technology with the type of bespoke service expected in physical stores. Meanwhile fine jewellery DTC brand Mejuri leverages digital styling appointments: “We’ve unlocked the barriers; it’s actually really successful for us, so we’re looking to expand it even further,” said co-founder and chief executive Noura Sakkijha. To be sure, having clarity on the role of each channel and the ways in which they interact will be key to leveraging existing strengths to bolster digital.

Humanise Digital

Digital does not mean the absence of human interaction between a jeweller and the customer. Rather, digital is yet another touchpoint to reach consumers and meet them where they are, whether that is through video on a digital screen or a chat conversation through SMS. “In China, e-commerce in the jewellery industry [has traditionally been] very, very transactional [but] there’s a lot more storytelling happening on Tmall today because, at the end of the day, it’s the biggest store window in the world,” said Jacques Roizen, Pandora’s senior vice president and general manager of China. “To treat it just purely as a transaction is a huge missed opportunity and that’s why we’ve made a lot of changes in upgrading our homepage [there].”

Incorporating human elements is not only key during the purchase, but also throughout post-purchase when customers need to have a means to celebrate and feel that they are treasured by the brand. As such, some brands and retailers, such as JD.com in China, are offering value-adds such as white glove delivery after a digital purchase, dedicated social media posts and personalised follow-ups. Closing the loop of one purchase with a personalised human touch lays positive groundwork for the next one.

ADVERTISEMENT

Given that nearly all fine jewellery purchases in the next five years will be influenced in some part by digital channels, sharpening and expanding omnichannel propositions will be key. As for digitally native players without a store network, we will increasingly see them complement their online offering with a small physical footprint, following in the footsteps of early digital natives like Blue Nile, Mejuri and Brilliant Earth, who have done so.

Mastering these elements will be a pre- requisite of building any compelling online offering. As a baseline, it will require a strategic assessment of channel roles and the use cases each channel should deliver. To be sure, commitment to e-commerce requires investment of time and resources in support of these use cases, but also a healthy dose of creativity to augment the digital environment with bold initiatives that authentically reflect the spirit of the brand. Digital offers significant potential to fine jewellery brands, but only if they engage with imagination, commitment and an open mind.

The inaugural edition of The State of Fashion: Watches and Jewellery report co-published by The Business of Fashion and McKinsey & Company forecasts a shake-up in priorities for hard luxury as well as different recovery scenarios across geographies and consumer segments. To learn more and download a copy of the report, click here.

BoF Professionals are invited to join us on July 13, 2021 for a special live event in which we'll unpack findings from the report. Register now to reserve your spot. If you are not a member, you can take advantage of our 30-day trial to experience all of the benefits of a BoF Professional membership.

Explore the six seismic shifts from the report:

The Future of Watches:

The Future of Jewellery:

Click here to explore more from this special edition report, including executive interviews.

The designer has always been an arch perfectionist, a quality that has been central to his success but which clashes with the demands on creative directors today, writes Imran Amed.

This week, Prada and Miu Miu reported strong sales as LVMH slowed and Kering retreated sharply. In fashion’s so-called “quiet luxury” moment, consumers may care less about whether products have logos and more about what those logos stand for.

The luxury goods maker is seeking pricing harmonisation across the globe, and adjusts prices in different markets to ensure that the company is”fair to all [its] clients everywhere,” CEO Leena Nair said.

Hermes saw Chinese buyers snap up its luxury products as the Kelly bag maker showed its resilience amid a broader slowdown in demand for the sector.