The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

This article first appeared in the special edition of The State of Fashion: Watches and Jewellery, co-published by The Business of Fashion and McKinsey & Company. To learn more and download a copy of the report, click here.

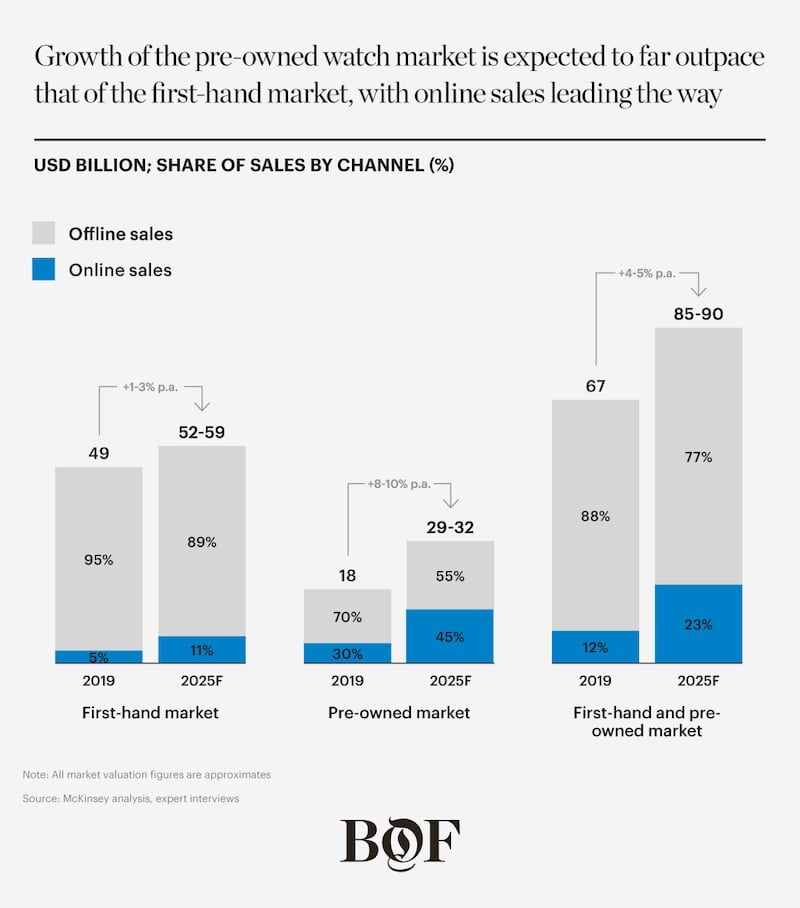

The pre-owned watch market is coming of age, with a growing number of brands, retailers and digital platforms consolidating the offering into a more secure and professional service than ever before. However, online players have been the real game-changer. Compared with just 5 percent in the new product space, 30 percent of pre-owned watches spanning the premium to ultra-luxury value segments are now sold online, as companies such as Watchfinder, Chrono24 and Chronext saw double-digit growth over recent years.

At the same time, consumers are showing increasing willingness to pay for pre-owned, with pre-owned watches now routinely selling at auctions for hundreds of thousands of dollars. McKinsey’s forecast expects the pre-owned market to expand by as much as 8 to 10 percent per year between 2019 and 2025, reaching annual sales of $29 to $32 billion, up from $18 billion in 2019. Comparatively, the new watch market for value segments from premium to ultra-luxury is predicted to grow just 1 to 3 percent annually during the same period.

One of the fastest-growing pre-owned markets is China, which has seen around 20 percent year-on-year expansion over the past four years, despite the underlying challenges that have traditionally plagued pre-owned in the country, owing to stigmas around resale and the value attributed to newness. This increase in demand is being driven by a golden combination of factors: increasing numbers of luxury shoppers, a culture of gift-giving, an appetite for distinctive style choices, the availability of advanced marketplaces (such as luxury resale platform Plum) and the proliferation of cutting-edge services, including specialist authentication and livestream sessions with celebrity hosts.

ADVERTISEMENT

Globally, rising demand for pre-owned watches has been driven by accelerating interest from younger consumers: some 30 percent of upper-income teens visited a pre-owned marketplace in late 2020, a rise of 5 percentage points from earlier in the year. This is on top of the changing perceptions of resale across other consumer categories, such as fashion, where the reframing of the second-hand narrative as “pre-loved” and a more sustainable buying choice has helped reduce the stigma of buying pre-owned items, particularly for younger consumers and those in territories where there is little vintage store culture.

While demand is rising, the intention behind pre-owned purchases is changing: pre-owned shoppers are no longer just looking for a good deal as a crop of new consumer types emerges. We now see three key customer types actively buying pre-owned: watch enthusiasts who are often looking for a particular model, year or edition; impatient shoppers who are turning to pre-owned to secure models that are limited in supply through traditional retail channels; and value seekers who are looking to purchase items or brands they otherwise would not have bought at full price, but have come to realise that pre-owned watches can be bought in as-new conditions for significant savings.

Watch enthusiasts and impatient shoppers, which together account for about two thirds of total pre-owned sales spanning all segments from premium to ultra-luxury, are most likely to be willing to pay a premium for a pre-owned watch. These consumers are typically searching for highly sought-after models that tend to command significant mark-ups from the retail price when sold as pre-owned — the Rolex Daytona, Patek Philippe Nautilus and Audemars Piguet Royal Oak are among this elite group of models, recently selling in the pre-owned market at premiums of 140 percent, 146 percent and 85 percent above their retail prices respectively. This class of watches sold at a premium has grown in importance in the pre-owned market, and while it makes up only 10 percent of pre-owned sales, it represents 40 percent of the revenue generated.

The remainder of pre-owned market sales are made up of watches sold at a discount, below first-hand retail value, which are often bought by value seekers who would otherwise not have access to them. As such, pre-owned offers an entry point into the brand.

Reflecting the broader consumer shift towards e-commerce and re-commerce specifically, the nexus of the current boom is digital marketplaces. From its headquarters in Germany Chrono24 has marched ahead of its rivals in recent years, listing some 186,000 watches on its marketplace, compared with just a few thousand on rival platforms. The platform attracts between 9 and 10 million unique visitors every month, said Chrono24 founder and co-chief executive Tim Stracke. “Watches is one of the few categories where the pieces stay alive for a long, long time... the value of stability we think always plays a certain role [in attracting customers],” he said.

Other third-party players have been keen to jump on the opportunity, creating a flurry of activity in the space. Most recently, US-based editorial and e-commerce watch platform Hodinkee entered the pre-owned segment, receiving $40 million in venture capital funding in December 2020, and later acquiring the online used luxury watch marketplace Crown & Caliber. Many luxury multi-category retailers, such as Vestiaire Collective, The RealReal and Rebelle, have added pre-owned watches to their assortment as well. While platforms originating from the watch category typically have a largely male and older customer base, multi-category players entering from fashion or jewellery, or with products at lower price points, may be able to capture younger segments and female consumers.

Though consumers have flooded onto pre-owned platforms, many mainstream brands have tended to sit on the sidelines. However, with the market growing at an unprecedented rate, brands’ time for waiting is over. With this significant opportunity comes significant risks in not engaging, in terms of the profit pool, relationships with customers, the ability to attract new consumers and market share. By actively participating in the pre-owned market, brands can open themselves up to the opportunity of “double dipping” on sales — once when sold first-hand, and again when taking a share of pre-owned sales. And while this model offers higher rewards for watches sold at higher price points, brands can benefit across the range of pre-owned offerings. Depending on the resale value, we estimate brands could capture an incremental 5 to 30 percent profit per product.

Among the companies already active in the pre-owned segment is Richemont — parent company of brands including Cartier, Vacheron Constantin and IWC — which acquired the Watchfinder platform in 2018 in a bid to develop its pre-owned business. Meanwhile, Richard Mille has partnered with the retailer Ninety to open a mono-brand shop dedicated to certified pre-owned and previous brand collections, while Audemars Piguet and MB&F are developing their pre-owned offerings either by allowing customers to trade in their old models in store, or by directly selling pre-owned watches within their own channels.

ADVERTISEMENT

To capitalise on the growing pre-owned opportunity, we have identified three strategies that business leaders should consider:

Integrate Pre-Owned Into the Brand Offering

Brand leaders could build an integrated pre-owned, mono-brand offering, leveraging both physical points of sale and direct online channels. To pursue this strategy, those who already have a DTC distribution strategy would need to believe that pre-owned is a long-term investment, and that integration is a route to building brand equity (for example through a superior customer experience). They also need to believe the “double dip” effect on margins will outweigh any risk of cannibalisation of first-hand sales. Audemars Piguet has already shown its willingness to engage in this strategy by allowing customers to trade in old models when buying new watches directly in its stores.

Enable Pre-Owned Sales in Third Party Channels

A second option would be to collaborate with multi-brand platforms to develop offerings such as shop-in-shops, certification and trade-in arrangements. Again, the investment would be predicated on an assumption that pre-owned is a long-term trend, that the current crop of platforms will continue to dominate and that brands can maintain a level of control over their representation while collecting a worthwhile percentage of sales. Business leaders must also believe there is an opportunity to boost sales of new watches by building brand equity. Third-party channels give brands some protection against cannibalisation, by avoiding like-for-like price comparison with first-hand watches in their store, making it a more attractive option for brands whose watches are mostly sold at a discount second-hand. Richemont’s integration of its brands into its subsidiary resale platform Watchfinder may make it harder to manage the full customer journey as one integrated experience, but it will allow Richemont a much broader access to the pre-owned market opportunity.

Invest in the Pre-Owned Market Opportunities

Brands can also invest in pre-owned market opportunities with or without engaging their own products. Using this approach, brands would likely acquire a stake in a multi-brand platform to benefit from the trend without needing to engage with their own products or brands. The underlying belief would be that second-hand is a transitory rather than a long-term trend, or that the pre-owned market is not a good fit for the brand, yet there may be a tactical opportunity to generate value.

Given the projected size of the market and rising consumer demand, the bottom line is that brands should now be proactively operating in the pre-owned market if they want to maintain control over their brand image and maximise customer touchpoints. Engaging more actively in pre-owned will also help brands extend their reach to new customer groups.

ADVERTISEMENT

From the perspective of platforms and independent retailers, increased brand engagement in pre-owned will likely lead to some erosion of their share of the pre-owned market, from 85 percent at present to around 70 percent by 2025. With this in mind, business leaders must think carefully about how they create a differentiated proposition.

While brands should choose engagement models that are aligned with their goals, those that participate directly will generate the biggest upside, with more control over brand representation and direct access to revenues. Many will also offer value-added services such as authentication and maintenance, helping to build trust, deepen engagement and encourage brand loyalty over time. Collectively, we expect brands to directly capture 25 percent of the pre-owned watch segment by 2025, representing $7 billion in incremental revenue. “The market has great potential,” said Michele Sofisti, the former chief executive of Girard-Perregaux. “If brands with a rich history focus on leveraging pre-owned to showcase brand heritage, you can create an interesting market.”

The inaugural edition of The State of Fashion: Watches and Jewellery report co-published by The Business of Fashion and McKinsey & Company forecasts a shake-up in priorities for hard luxury as well as different recovery scenarios across geographies and consumer segments. To learn more and download a copy of the report, click here.

BoF Professionals are invited to join us on July 13, 2021 for a special live event in which we'll unpack findings from the report. Register now to reserve your spot. If you are not a member, you can take advantage of our 30-day trial to experience all of the benefits of a BoF Professional membership.

Explore the six seismic shifts from the report:

The Future of Watches:

The Future of Jewellery:

Click here to explore more from this special edition report, including executive interviews.

The former CFDA president sat down with BoF founder and editor-in-chief Imran Amed to discuss his remarkable life and career and how big business has changed the fashion industry.

Luxury brands need a broader pricing architecture that delivers meaningful value for all customers, writes Imran Amed.

Brands from Valentino to Prada and start-ups like Pulco Studios are vying to cash in on the racket sport’s aspirational aesthetic and affluent fanbase.

The fashion giant has been working with advisers to study possibilities for the Marc Jacobs brand after being approached by suitors.